Summary

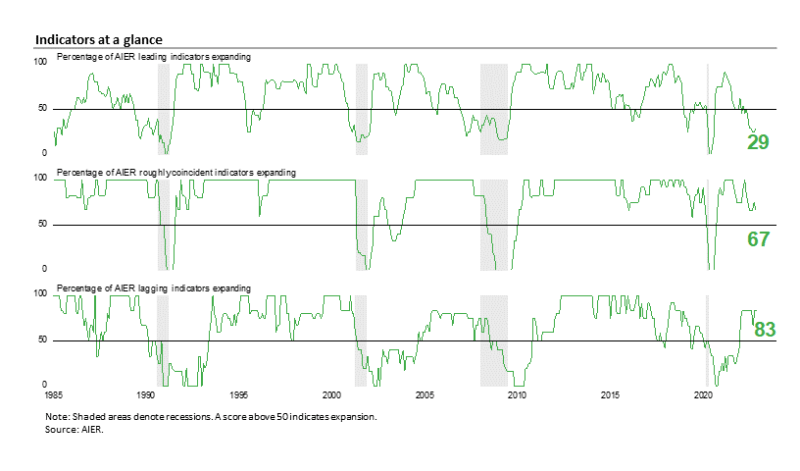

AIER’s Leading Indicators Index rose to 29 in November versus 25 in October. Despite the slight improvement, the latest result is the sixth consecutive month below the neutral 50 threshold. The low readings are consistent with weakness in the economy and significantly elevated risks for the outlook.

Payrolls continue to expand, and consumer price increases continue at an elevated pace, both in the face of an aggressive Fed tightening cycle. The strong job market boosts consumers’ views of current conditions while rising interest rates and elevated rates of price increases depress consumers’ expectations for the future. With interest rates already taking a toll on housing, consumer spending and business decisions on hiring and investment remain critical to the economic outlook.

The longer elevated rates of price increases continue and the higher the Fed raises interest rates, the higher the probability that consumers and businesses retrench. Overall, the outlook remains highly uncertain. Caution is warranted.

AIER Leading Indicators Index Rises to 29 in November, But Still Signals Significant Risks

The AIER Leading Indicators index improved slightly in November, rising to 29 from 25 in October. The November result is still down 63 points from the March 2021 high of 92. With the latest reading holding well below the neutral 50 threshold for the sixth consecutive month, the AIER Leading Indicators Index is signaling economic weakness and significantly elevated outlook risks.

One leading indicator changed signal in November. The real retail sales indicator improved from a negative trend to a neutral trend. This indicator has been volatile recently, changing signals seven times in the last twelve months. The indicator showed a positive trend in three months, a negative trend in two months, and flat trend in seven months. Indicators often become volatile around inflection points.

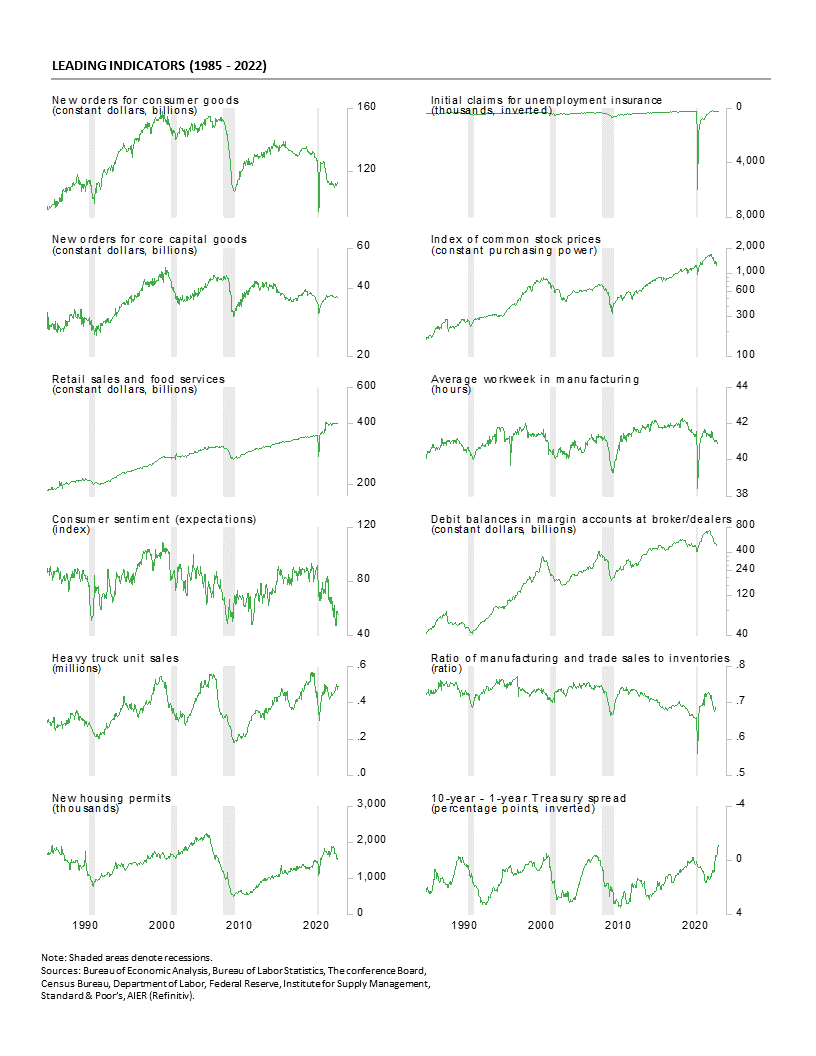

Among the 12 leading indicators, three were in a positive trend in November – real new orders for consumer goods, heavy truck unit sales, and the ten-year – one-year treasury spread, nine were trending lower – initial claims for unemployment claims, the average workweek in manufacturing, manufacturing and trade sales to inventories ratio, the University of Michigan Index of Consumer Expectations, real new orders for nondefense capital goods excluding aircraft, housing permits, real stock prices, and debit balances in margin accounts, and one – real retail sales and food services – was trending flat or neutral.

The Roughly Coincident Indicators index weakened in November, falling back to 67 after a 75 in October and three consecutive months at 67 from July through September. Before the three-month run at 67, the indicator posted a 75 in June, 83 in May, and a perfect 100 in April. The Roughly Coincident Indicators Index has been above the neutral 50 threshold since October 2020.

One indicator changed signal last month. The employment-to-population ratio indicator weakened to a neutral trend from a positive trend in the prior month. This indicator had been in a positive trend for 22 consecutive months.

In total, three roughly coincident indicators – nonfarm payrolls, real personal income excluding transfers, and industrial production – were trending higher in November while the real manufacturing and trade sales indicator and the employment-to-population ratio indicator were in neutral trends, and the Conference Board Consumer Confidence in the Present Situation indicator was in a negative trend. Given the poor performance of the AIER Leading Indicators Index, it would not be surprising to see declines in the Roughly Coincident Index in the coming months.

AIER’s Lagging Indicators index held at 83 in November. The Lagging Indicators Index has been relatively steady, posting a reading of 83 for nine of the last ten months. The exception was a dip to 67 in September. In total, five indicators – the duration of unemployment indicator, the real manufacturing and trade inventories indicator, the composite short-term interest rates indicator, the 12-month change in the core Consumer Price Index indicator, and the commercial and industrial loans indicator – were in favorable trends. One indicator, real private nonresidential construction, had an unfavorable trend.

Overall, the AIER Leading Indicators Index remained well below neutral in the latest month, signaling economic weakness and sharply elevated risks for the outlook. The economy continues to face significant headwinds from elevated rates of price increases and an aggressive Fed tightening cycle. With rising interest rates already hitting the housing market, the strength of the labor market becomes an even more critical component of the economic outlook. Continued jobs gains provide support for consumers’ positive views of current economic conditions and help sustain consumer spending. However, elevated rates of price increases and rising interest rates weigh on consumer expectations for the future. If significant declines in payrolls begin to occur, support for consumer spending would likely fade, resulting in an economic contraction. If price increases slow and the Fed eases back on policy, domestic demand growth would likely reaccelerate.

Fed policy is likely to be a key variable in the progression of price pressures and the labor market. Furthermore, the fallout from the Russian invasion of Ukraine and periodic lockdowns in China continue to boost uncertainty. Caution is warranted.

Housing Market Outlook Darkens

Total housing starts fell to a 1.425 million annual rate in October from a 1.488 million pace in September, a 4.2 percent drop. From a year ago, total starts are down 8.8 percent. Total housing permits also fell in October, posting a 2.4 percent drop to 1.526 million versus 1.564 million in September. Total permits are down 10.1 percent from the October 2021 level.

Starts in the dominant single-family segment posted a rate of 855,000 in October versus 911,000 in September, a drop of 6.1 percent. That is the fourth consecutive month under one million and the slowest pace since May 2020. Starts are down 20.8 percent from a year ago. Single-family permits fell 3.6 percent to 839,000 versus 870,000 in September, the fifth consecutive month under one million and the slowest pace since May 2020.

Starts of multifamily structures with five or more units decreased 0.5 percent to 556,000 but are up 17.3 percent over the past year, while starts for the two- to four-family-unit segment fell 22.2 percent to a 14,000-unit pace versus 18,000 in September. Total multifamily starts were off 1.2 percent to 570,000 in October but still showing a gain of 17.8 percent from a year ago.

Multifamily permits for the 5-or-more group dropped by 1.9 percent to 633,000, while permits for the two-to-four-unit category increased 10.2 percent to 54,000. Total multifamily permits were 687,000, down 1.0 percent for the month but up 10.6 percent from a year ago.

Meanwhile, the National Association of Home Builders’ Housing Market Index, a measure of homebuilder sentiment, fell again in November, coming in at 33 versus 38 in October. That is the eleventh consecutive drop and the fourth consecutive month below the neutral 50 threshold. The index is down sharply from recent highs of 84 in December 2021 and 90 in November 2020.

All three components of the Housing Market Index fell again in November. The expected single-family sales index dropped to 31 from 35 in the prior month, the current single-family sales index was down to 39 from 45 in October, and the traffic of prospective buyers index sank again, hitting 20 from 25 in the prior month.

Input costs and supply delivery problems are still concerns for builders though lumber prices have declined sharply from recent highs. Lumber recently traded around $430 per 1,000 board feet in mid-November, down from peaks around $1,700 in May 2021 and $1,500 in early March 2022.

Mortgage rates continue to surge, with the rate on a 30-year fixed rate mortgage coming in at 7.08 percent in mid-November. Rates are up more than 400 basis points, more than double the lows in early 2021.

Retail Spending Was Strong in October, but the Trend Is Flat

Total nominal retail sales and food-services spending rose 1.3 percent in October after being unchanged in September. From a year ago, retail sales are up 8.3 percent and remain well above the pre-pandemic trend.

Nominal retail sales excluding motor vehicle and parts dealers and gasoline stations – or core retail sales – rose 0.9 percent in October following a 0.6 percent gain in September. From October 2021 to October 2022, core retail sales are up 8.0 percent. As with total retail sales, core retail sales remain well above the pre-pandemic trend.

However, these data are not adjusted for price changes. In real terms (adjusted using the CPI), real total retail sales were up 0.8 percent in October following a 0.4 percent decrease in September and declines in five of the last eight months. From a year ago, real total retail sales are up 0.5 percent versus a ten-year annualized growth rate of 2.5 percent from 2010 through 2019. As with nominal retail sales, real retail sales remain well above their pre-pandemic trend, but since March 2021, they have been trending flat.

Real core retail sales posted a 0.6 percent rise in October after being unchanged in September. Over the last twelve months, real core retail sales are up 1.6 percent versus a ten-year annualized growth rate of 2.2 percent from 2010 through 2019. While real total retail sales are still below the March 2021 peak, real core retail sales have been trending higher at a rate of 1.6 percent per year.

Categories were generally higher in nominal terms for the month, with nine up and four down in October. The gains were led by gasoline spending, with a 4.1 percent jump following a 3.7 percent drop in September. The average price for a gallon of gasoline was $4.13, up 3.5 percent from $3.99 in September, suggesting price changes more than accounted for most of the rise. Food services and drinking places (restaurants) rose 1.6 percent followed by food and beverage store sales (groceries) up 1.4 percent, motor vehicles and parts retailers, (1.3 percent), nonstore retailers (1.2 percent), furniture and home furnishings (1.1 percent), and building materials, gardening equipment and supplies (1.1 percent). Declines came in electronics and appliance stores (-0.3 percent), sporting goods, hobby, musical instruments, and book stores (-0.3 percent), and general merchandise stores (-0.2 percent).

Overall, nominal total and core retail sales remain well above trend. However, rising prices are still providing a significant boost to the numbers. In real terms, total and core retail sales posted solid gains in October, but the trends are much weaker. Retail spending measured as a share of personal income remains well above the average shares seen in the 2010 through 2019 period and the 1992 through 2007 period.

Payroll Gains Beat Expectations, but the Pace Is Slowing

Total nonfarm payrolls posted a 263,000 gain in November versus a 284,000 rise in October (revised up by 23,000), while September had an increase of 269,000 (revised down by 46,000). The November result easily beat the consensus expectation of 200,000. However, the gain is still the slowest since April 2021.

Excluding the government sector, private payrolls posted a gain of 221,000 in November following the addition of a net 248,000 jobs in October. The average monthly gain over the 23 months since January 2021 was 449,000. However, the monthly increases appear to be slowing. Over the 14 months from January 2021 through February 2022, the average monthly rise was 535,000; for the five months from March 2022 through July 2022, the average was 376,000; and over the last four months, the average has dropped to 239,000. Despite beating expectations, the trend in payroll gains is slowing.

Furthermore, the results among the various industries were mixed in November, with just two industry groups, healthcare and leisure, accounting for 70 percent of the net gain for the month. Four industries had payroll declines in November.

Within the 221,000 increase in private payrolls, private services added 184,000 versus a 12-month average of 322,300, while goods-producing industries added 37,000 versus a 12-month average of 60,400.

Within private service-producing industries, leisure and hospitality added 88,000 (versus a 90,300 twelve-month average), education and health services increased by 82,000 (versus 77,700), information added 19,000 (versus 13,400), and financial gained 14,000 (versus 12,300).

Within the 37,000 addition in goods-producing industries, construction added 20,000, durable-goods manufacturing rose by 11,000, nondurable-goods manufacturing expanded by 3,000, and mining and logging industries added 3,000.

While a few of the services industries dominate actual monthly private payroll gains, monthly percent changes paint a different picture. Gains and losses were more evenly distributed, as three industries gained at least 0.5 percent, but four had declines.

Average hourly earnings for all private workers also had a bigger gain than expected, rising 0.6 percent in November, the third consecutive acceleration in growth. That puts the 12-month gain at 5.1 percent, down from a recent peak of 5.6 percent in March 2022. Average hourly earnings for private, production and nonsupervisory workers rose 0.7 percent for the month and are up 5.8 percent from a year ago, down from 6.7 percent in March.

The average workweek for all workers fell to 34.4 hours in November from 34.5 in October while the average workweek for production and nonsupervisory dropped to 33.9 hours versus 34.0 in the prior month.

Combining payrolls with hourly earnings and hours worked, the index of aggregate weekly payrolls for all workers gained 0.5 percent in November and is up 7.6 percent from a year ago; the index for production and nonsupervisory workers rose 0.6 percent and is 8.7 percent above the year ago level.

The total number of officially unemployed was 6.011 million in November, a drop of 48,000. The unemployment rate was unchanged at 3.7 percent, while the underemployed rate, referred to as the U-6 rate, decreased by 0.1 percentage points to 6.7 percent in November. Both measures have been bouncing around in a flat trend over the last few months.

The employment-to-population ratio, one of AIER’s Roughly Coincident indicators, came in at 59.9 percent for November, down 0.1 from October, the second consecutive drop and still significantly below the 61.2 percent in February 2020.

The labor force participation rate also fell by 0.1 percentage point in November to 62.1 percent. This important measure has been trending flat recently but is still well below the 63.4 percent of February 2020.

The total labor force came in at 164.481 million, down 186,000 from the prior month and nearly matching the February 2020 level. If the 63.4 percent participation rate were applied to the current working-age population of 264.708 million, an additional 3.34 million workers would be available.

The November jobs report shows total nonfarm and private payrolls posted additional albeit slower gains than recent prior periods. Despite beating expectations in November that some might interpret as a “strong labor market,” the data show the trend in payroll gains is decelerating. Furthermore, concerns about future payroll gains persist in light of aggressive Fed interest rate increases, a modest upward trend in initial claims for unemployment insurance, and an increase in job cut announcements. Still, the level of open jobs remains high, and the number of available workers is low, suggesting the labor market remains tight.

Weekly Initial Claims Continue to Trend Higher

Initial claims for regular state unemployment insurance fell by 16,000 for the week ending November 26th, coming in at 225,000. The previous week’s 241,000 was revised up from the initial estimate of 240,000. The four-week average of weekly initial claims rose to 228,750, up 1,750 for the week. That was the fifth increase in the last seven weeks and the highest level since September 3rd.

When measured as a percentage of nonfarm payrolls, claims came in at 0.140 percent for October, up from 0.136 in September and above the record low of 0.117 in March. While the level of weekly initial claims for unemployment insurance remains very low by historical comparison, the rising trend is a concern. Furthermore, job-cut announcements have started to increase recently, adding to the concern over the rising trend in initial claims.

The number of ongoing claims for state unemployment programs totaled 1.338 million for the week ending November 12th, an increase of 111,080 from the prior week. State continuing claims are at the highest level since August 27th but remain within the 1.2 million and 1.5 million range.

The latest results for the combined Federal and state programs put the total number of people claiming benefits in all unemployment programs at 1.368 million for the week ended November 12th, an increase of 115,477 from the prior week.

While the overall low level of initial claims suggests the labor market remains tight, the upward trend in claims and rising job-cut announcements are concerns. The tight labor market is a crucial component of the economy, providing support for consumer spending. However, persistently elevated rates of price increases already weigh on consumer attitudes, and if consumers lose confidence in the labor market, they may significantly reduce spending. The outlook remains highly uncertain.

Private-Sector Job Openings Remain High Despite Falling in October

The latest Job Openings and Labor Turnover Survey from the Bureau of Labor Statistics shows the total number of job openings in the economy decreased to 10.334 million in October, down from 10.687 million in September.

The number of open positions in the private sector decreased to 9.412 million in October, down from 9.627 million in September. October was the fifth decline in the last seven months since hitting a record high in March.

The total job openings rate, openings divided by the sum of jobs plus openings, fell to 6.3 percent in October from 6.5 percent in September, while the private-sector job-openings rate decreased to 6.7 percent from 6.9 percent in the previous month. The October result for the private sector is 1.0 percentage points below the March peak.

The industries with the highest openings are education and health care (2.172 million), professional and business services (1.794 million), trade, transportation, and utilities (1.644 million), and leisure and hospitality (1.578 million). The highest openings rates were in leisure and hospitality (9.0 percent), education and health care (8.1 percent), and professional and business services (7.4 percent).

The number of private-sector quits declined for a second consecutive month in October, coming in at 3.792 million, down from 3.819 million in September. Trade, transportation, and utilities led with 904,000 quits, followed by leisure and hospitality with 869,000 quits, and by professional and business services with 655,000.

The private-sector quits rate held steady at 2.9 percent in October. The private-sector quits rate is the lowest since March 2021 and 0.5 percentage points below the record high of 3.4 percent in November 2021.

Private-sector layoffs and discharges rose in the latest month, rising to 1.314 million, up from 1.247 million in September. The trend in layoffs and discharges may be higher since hitting a low of 1.183 million in December 2021. The private-sector layoffs and discharge rate held steady in October, coming in at 1.0 percent, above the 0.9 percent low in December 2021.

The number of job seekers (unemployed plus those not in the labor force but who want a job) per opening ticked up slightly in October, rising to 1.095 from 1.083 in September. Before the lockdown recession, the low was 1.409 in October 2019.

Today’s job openings data suggest the labor market maintained resilience through October. While the low number of available workers per opening implies the labor market remains tight, some deterioration at the margin is a warning sign. Caution is warranted.

Related Posts

Operation Chokepoint 2.0: The Crypto Crackdown Explained (Video)

In this episode of Liberty Curious, Kate Wand discusses the Obama-era Operation Chokepoint, and today’s “Operation Chokepoint 2.0” with AIER Senior Research Faculty Thomas Hogan. Tom explains how government regulators […]

Earth Day, Waste and Productive Complements

It has been just over half a century since the first Earth Day in 1970. Over that time, April 22 has turned into a day with lots of waste cleanup […]

Focusing Exclusively on “Creating Jobs” Can Do More Harm Than Good

We are constantly bombarded by politicians declaring the importance of “creating jobs” in the economy. We regularly see government initiatives like public works projects, “stimulus” programs, and government subsidies enacted […]