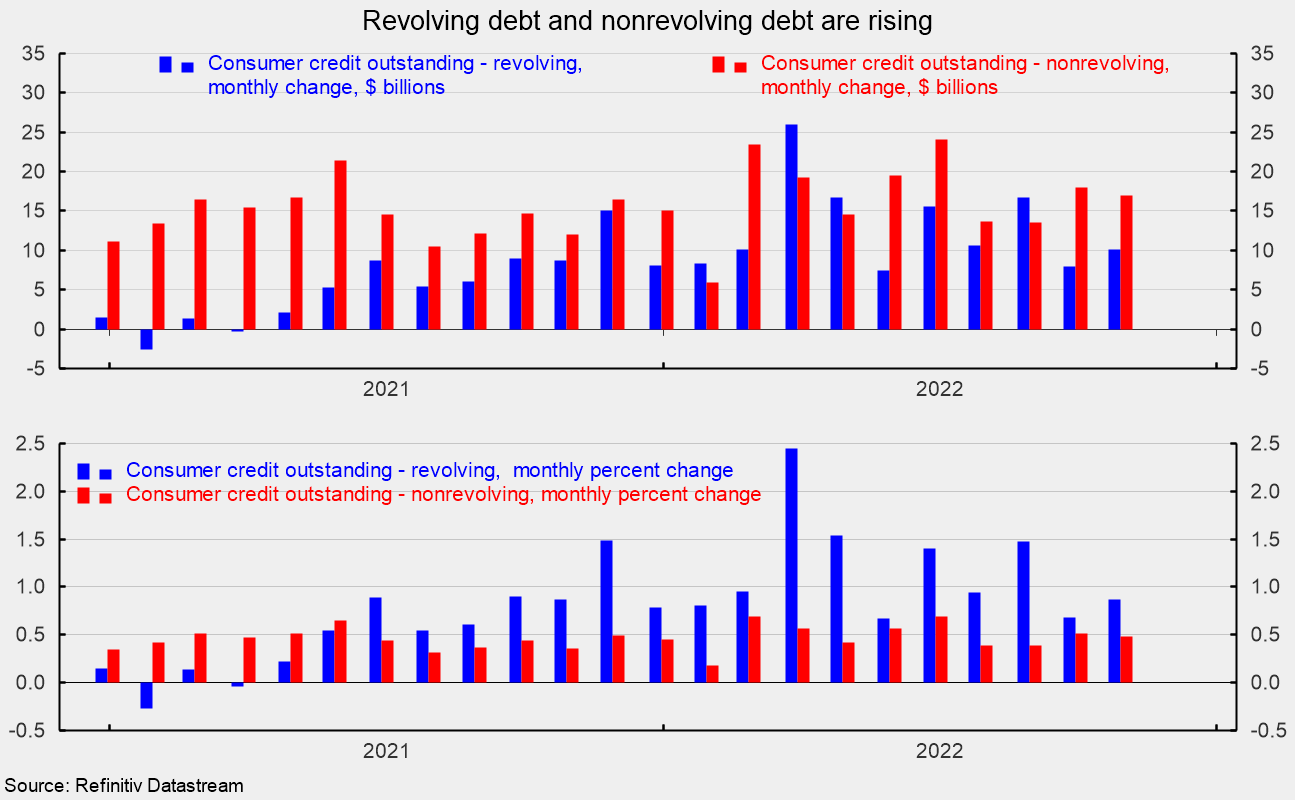

Total consumer credit outstanding rose by $27.1 billion to $4,729.3 billion in October, a 0.6 percent increase from the prior month. From a year ago, total consumer credit is up 8.1 percent, the fastest pace since November 2011 (see first chart).

Within the total, revolving credit, primarily credit cards, added $10.1 billion (see top of second chart) to $1,171.2 billion, a 0.9 percent gain for the month and a 15.0 percent rise over the past year. Nonrevolving credit added $17.0 billion (see top of second chart) to come in at $3,558.2 billion, a 0.5 percent gain for the month and a 6.0 percent gain from a year ago. Revolving credit made up 24.8 percent of total consumer credit while nonrevolving accounted for 75.2 percent.

Nonrevolving credit has been growing rapidly over the past decade and a half, driven primarily by student loans and motor vehicle loans. As of the end of the third quarter, student loans totaled $1,768.8 billion, or 49.7 percent of nonrevolving credit, and auto loans totaled $1,397.0 billion, or 39.2 percent of nonrevolving debt. Together, they account for 88.9 percent of nonrevolving debt outstanding and 67.3 percent of total consumer credit.

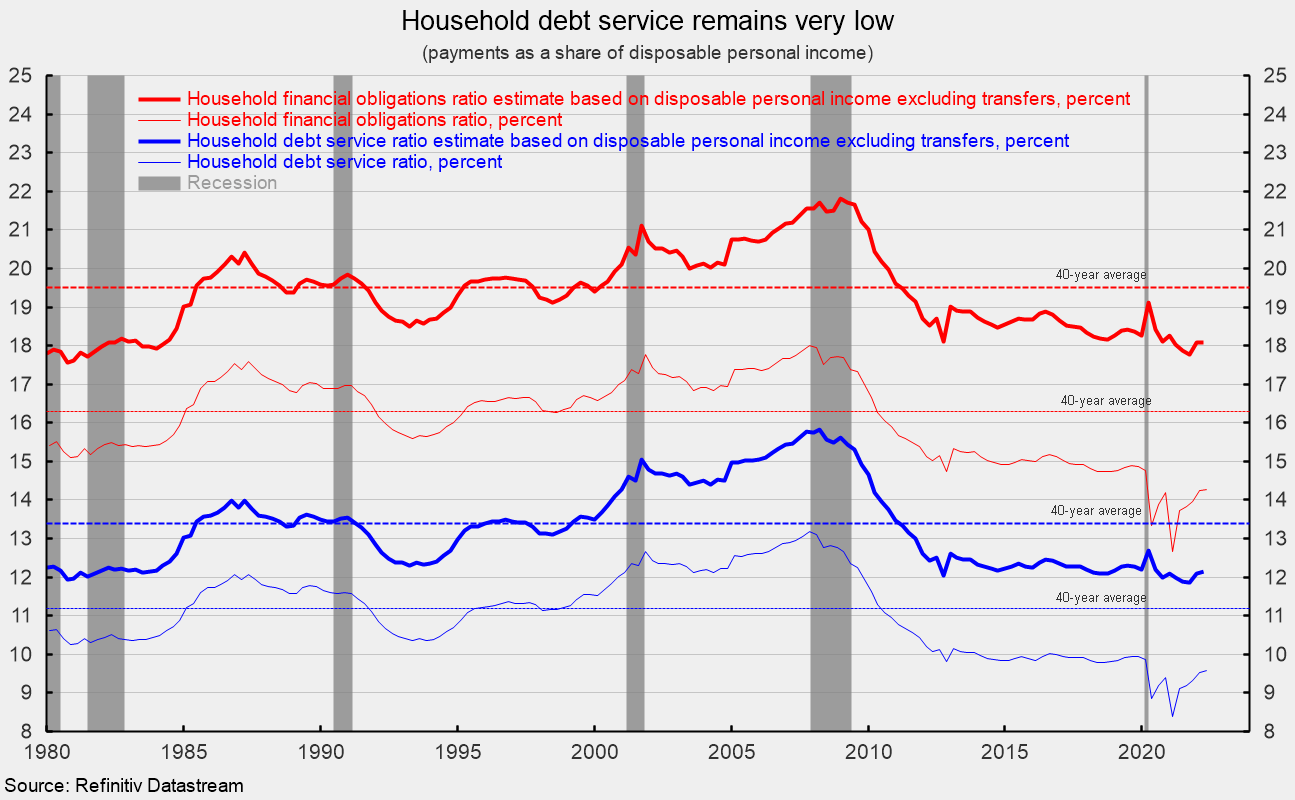

Despite the rise in consumer debt, two key measures suggest that household balance sheets are generally healthy. As of the second quarter, the financial obligations ratio (monthly payments for financial obligations as a share of disposable personal income) was 14.27 percent, up from 14.24 percent in the prior quarter. Like many economic statistics, these numbers have been heavily distorted by the pandemic, lockdowns, and government payments. Excluding the government transfer payments, financial obligations would be 18.1 percent, unchanged from the prior quarter. Both measures remain well below their 40-year average through the end of 2019 (see third chart).

Household debt service (a narrower measure that includes just minimum monthly debt payments) came in at 9.58 percent for the second quarter, up from 9.52 percent. Excluding the government transfer payments, debt service comes in at 12.14 percent. Both of these measures are also well below their 40-year average (see third chart).

Total consumer credit rose again in October on gains in revolving credit and nonrevolving credit. Growth has been accelerating and when combined with rising interest rates, may push financial burdens up from the current low levels. Any significant decline in the labor market and personal incomes will only exacerbate the trend.

Related Posts

Operation Chokepoint 2.0: The Crypto Crackdown Explained (Video)

In this episode of Liberty Curious, Kate Wand discusses the Obama-era Operation Chokepoint, and today’s “Operation Chokepoint 2.0” with AIER Senior Research Faculty Thomas Hogan. Tom explains how government regulators […]

Earth Day, Waste and Productive Complements

It has been just over half a century since the first Earth Day in 1970. Over that time, April 22 has turned into a day with lots of waste cleanup […]

Focusing Exclusively on “Creating Jobs” Can Do More Harm Than Good

We are constantly bombarded by politicians declaring the importance of “creating jobs” in the economy. We regularly see government initiatives like public works projects, “stimulus” programs, and government subsidies enacted […]