The preliminary December results from the University of Michigan Surveys of Consumers show overall consumer sentiment rebounded slightly in early December but remains well below pre-pandemic levels. Rising prices remain a key driver of overall sentiment.

Consumer sentiment increased to 70.4 in early December, up from 67.4 in November (see first chart), a gain of 4.5 percent. The index remains 12.8 percent below the year ago level and 27.6 percent below the 2018 – 2019 average (see second chart).

The current-economic-conditions index rose to 74.6 from 73.6 in November (see first chart). That is a 1.4 percent increase but leaves the index with a 17.1 percent decrease from December 2020 and a 33.7 percent decline from the 2018 – 2019 average (see second chart).

The second sub-index — that of consumer expectations, one of the AIER leading indicators — added 4.3 points or 6.8 percent for the month, rising to 67.8 (see first chart). The index is off 9.1 percent from a year ago and 22.3 percent from its 2018 – 2019 average (see second chart).

According to the report, “When directly asked whether inflation or unemployment was the more serious problem facing the nation, 76% selected inflation while just 21% selected unemployment (the balance reported the problems were equal or they couldn’t choose).” The report goes on to add, “The dominance of inflation over unemployment was true for all income, age, education, region, and political subgroups.”

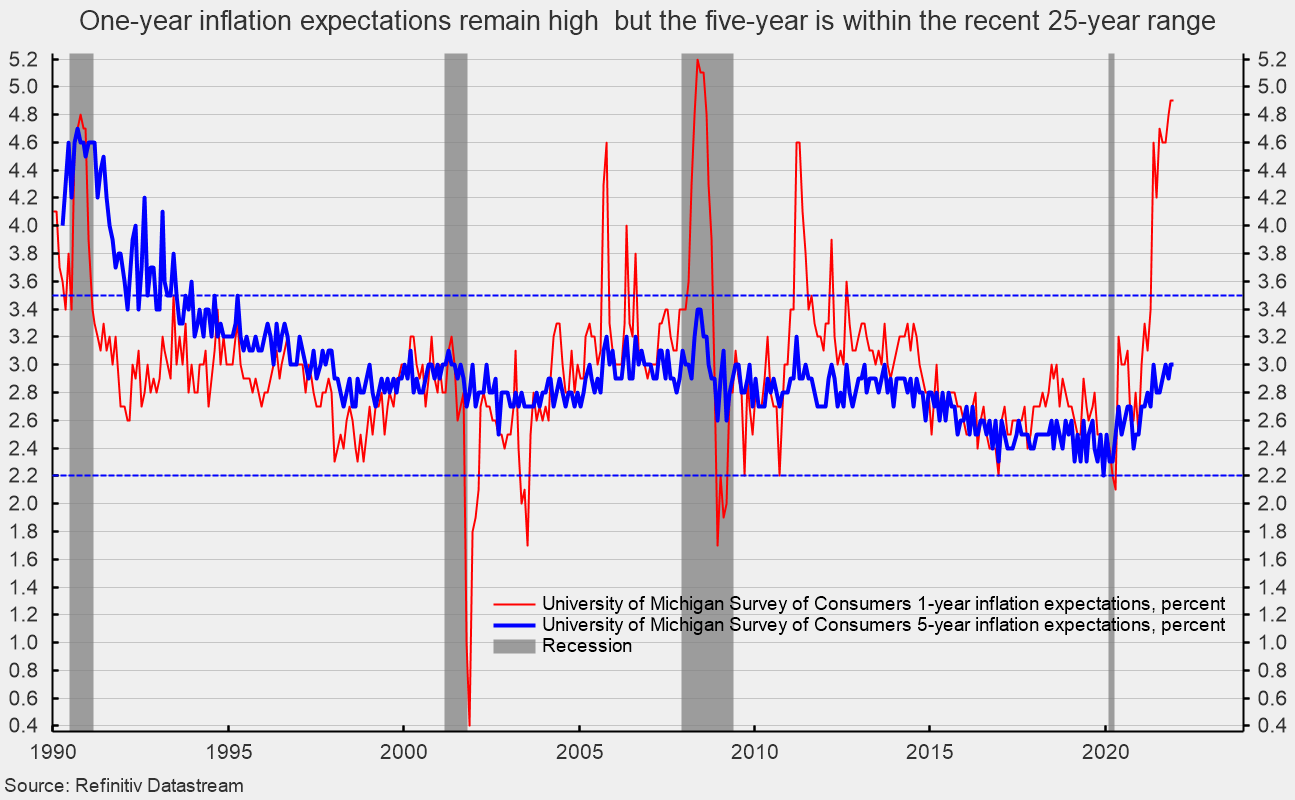

The one-year inflation expectations held at 4.9 percent in early December, maintaining the highest level since hitting 5.1 percent in July 2008. The one-year expectation has spiked above 3.5 percent several times since 2005 only to fall back (see third chart). The five-year inflation expectation remained unchanged at 3.0 percent in early December. That result remains well within the 25-year range of 2.2 percent to 3.5 percent (see third chart).

Another key result from the early December survey was the notable divisions among income cohorts. According to the report, “The more interesting result was the large disparity between monthly gain among households with incomes in the lowest third (+23.6%) of the income distribution compared with the modest losses among households in the middle (-3.8%) and top third (-4.3%). While small differences in the direction of change are rather common, it is quite unusual to record such a large change in the bottom third: a larger one-month percentage was recorded only once before, a gain of 29.2% in June 1980. While it is usually assumed that such extreme changes represent an erroneous result due to small samples, in 1980 it was the households in the bottom income third that initially signaled the end of the first part of the double recession in 1980-82, with upper income households following in subsequent months.” The report adds, “While consumers’ evaluations of their current and prospective financial situation have both declined, for the first time there has been a substantial gap between the two assessments. The decline in how consumers have judged their current financial situation was half as large as the decline in how they judged their future financial prospects. The split is presumably due to the impact of the cash stimulus and unemployment payments. Future financial evaluations have been lessened primarily by rising inflation as nearly half of all consumers expect falling inflation-adjusted incomes during the year ahead.”

Despite the increase in early December, the persistent weak readings in consumer sentiment reflect the impact of higher consumer prices. The surge in prices for many consumer goods and services is largely a function of shortages of materials, a tight labor market, and logistical issues that prevent supply from meeting demand. Price pressures will ease as production returns to normal and logistical issues are resolved, but the process may take an extended period.

Related Posts

Operation Chokepoint 2.0: The Crypto Crackdown Explained (Video)

In this episode of Liberty Curious, Kate Wand discusses the Obama-era Operation Chokepoint, and today’s “Operation Chokepoint 2.0” with AIER Senior Research Faculty Thomas Hogan. Tom explains how government regulators […]

Earth Day, Waste and Productive Complements

It has been just over half a century since the first Earth Day in 1970. Over that time, April 22 has turned into a day with lots of waste cleanup […]

Focusing Exclusively on “Creating Jobs” Can Do More Harm Than Good

We are constantly bombarded by politicians declaring the importance of “creating jobs” in the economy. We regularly see government initiatives like public works projects, “stimulus” programs, and government subsidies enacted […]