The final April results from the University of Michigan Surveys of Consumers show overall consumer sentiment bounced higher in April after hitting a multiyear low in March (see top of first chart). The gain was almost entirely due to a jump in consumer expectations for the future. The composite consumer sentiment increased to 65.2 in April, up from 59.4 in March, a gain of 5.8 points or 9.8 percent. The index is still down 35.8 points from the February 2020 peak.

The current-economic-conditions index rose to 69.4 from 67.2 in March (see the middle of the first chart). That is a 2.2-point or 3.3 percent gain for the month but still leaves the index with a 45.4-point drop since February 2020.

The second sub-index — that of consumer expectations, one of the AIER leading indicators — jumped 8.2 points or 15.1 percent for the month, rising to 62.5 (see bottom of first chart). The index is still off 29.6 points since February 2020.

All three indexes remain below the lows seen at the onset of four of the last six recessions (see first chart).

According to the report, “Most of the surge was concentrated in expectations, with gains of 21.6% in the year-ahead outlook for the economy and an 18.3% jump in personal financial expectations. The cause was a sharp drop in gas price expectations, falling to just 0.4 cents from last month’s 49.6. The overall impact on sentiment trends, however, was quite small: other than the last two months, the Sentiment Index in April was still lower than in any prior month in the past decade.” The report goes on to add, “The downward slide in confidence represents the impact of uncertainty, which began with the pandemic and was reinforced by cross-currents, including the negative impact of inflation and higher interest rates, and the positive impact of a persistently strong labor market and rising wages. The global economy has added even more uncertainties about prospects for the U.S. economy, including the growing involvement in the military support for Ukraine, and renewed supply line disruptions from the covid crisis in China. Who would not be apprehensive about future conditions, even if on balance they anticipated a continued expansion?”

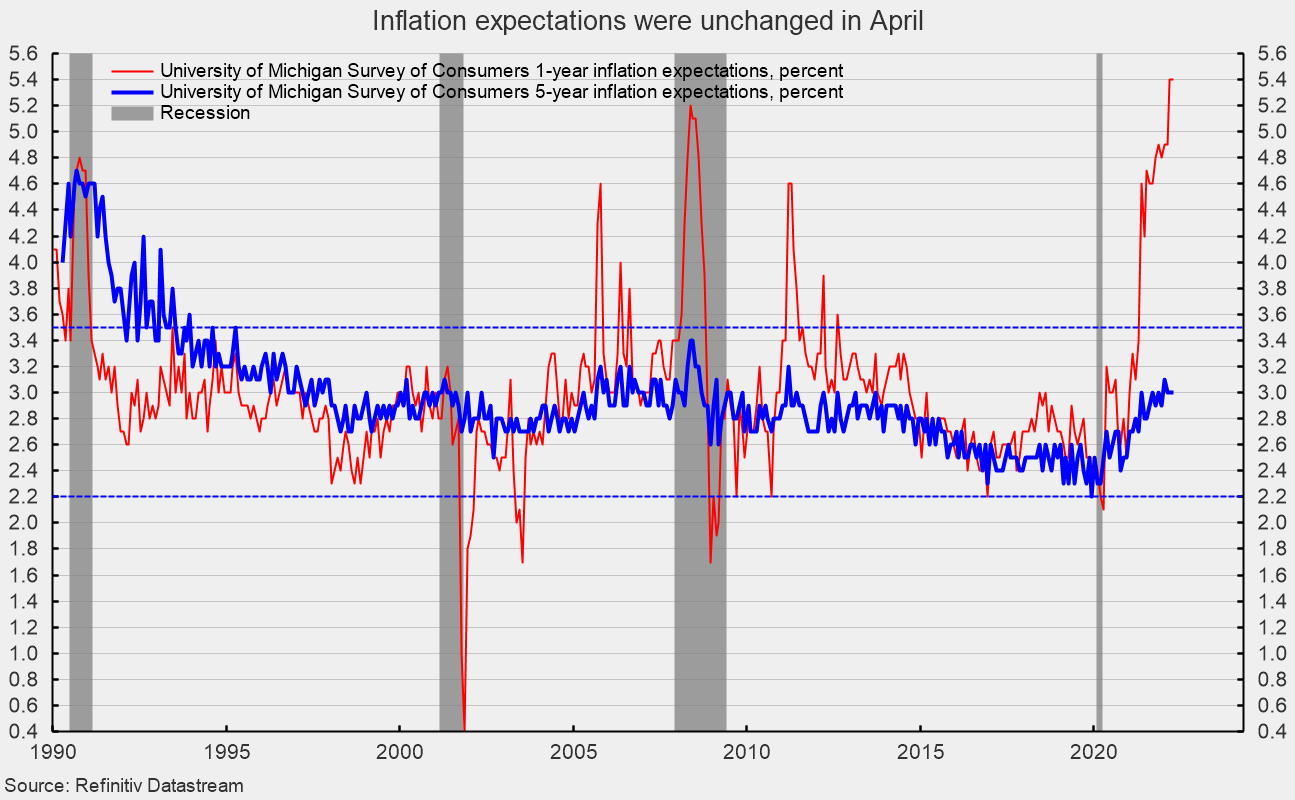

The one-year inflation expectations was unchanged at 5.4 percent in April, the highest level since November 1981. The one-year expectations has spiked above 3.5 percent several times since 2005 only to fall back (see second chart). The five-year inflation expectations remained unchanged at 3.0 percent in April. That result remains well within the 25-year range of 2.2 percent to 3.5 percent (see second chart).

According to the report, “Moreover, consumers have lost confidence in economic policies, with fiscal actions increasingly hampered by partisanship in the runup to the Congressional elections. Monetary policy now aims at tempering the strong labor market and trimming wage gains, the only factors that now support optimism.”

The report concludes, “The goal of a soft landing will be more difficult to achieve given the uncertainties that now prevail, raising prospects for a halt, or even a temporary reversal, in the Fed’s interest rate policies. The probability of consumers reaching a tipping point will increasingly depend on prospects for a strong labor market and continued wage gains. The cost of that renewed strength is an accelerating wage-price spiral.”

Economic risks remain elevated due to the Russian invasion of Ukraine, persistently high inflation, and the start of a Fed tightening cycle which is likely to undermine the strongest support of consumer sentiment and consumer spending, the strong labor market. Furthermore, the ramping up of negative political ads as the midterm elections approach may also weigh on consumer sentiment in coming months. The overall economic outlook remains highly uncertain.

Related Posts

Operation Chokepoint 2.0: The Crypto Crackdown Explained (Video)

In this episode of Liberty Curious, Kate Wand discusses the Obama-era Operation Chokepoint, and today’s “Operation Chokepoint 2.0” with AIER Senior Research Faculty Thomas Hogan. Tom explains how government regulators […]

Earth Day, Waste and Productive Complements

It has been just over half a century since the first Earth Day in 1970. Over that time, April 22 has turned into a day with lots of waste cleanup […]

Focusing Exclusively on “Creating Jobs” Can Do More Harm Than Good

We are constantly bombarded by politicians declaring the importance of “creating jobs” in the economy. We regularly see government initiatives like public works projects, “stimulus” programs, and government subsidies enacted […]