The Institute for Supply Management’s composite services index rose to 61.9 percent in September, gaining 0.2 points from 61.7 percent in the prior month. The index remains well above neutral and suggests the 16th consecutive month of expansion for the services sector and the broader economy (see top of first chart).

Among the key components of the services index, the business-activity index (comparable to the production index in the ISM manufacturing report) increased to 62.3 percent in September, up from 60.1 percent in August, a gain of 2.2 points (see top of first chart). This measure has been above 50 percent for 16 consecutive months and above 60 percent for the last seven months. For September, 17 industries in the services survey reported expansion versus one reporting contraction.

The services new-orders index rose to 63.5 percent from 63.2 percent in August, a gain of 0.3 percentage points from August (see bottom of first chart). Similar to the activity index, new orders have been above 50 percent for 16 months and above 60 for the past seven months – a strong performance overall. For September, 17 industries reported expansion in new orders in September while one reported a drop.

The new-export-orders index, a separate index that measures only orders for export, fell back slightly to 59.5 percent in September versus 60.6 percent in August. Eleven industries reported growth in export orders against just two reporting declines.

Backlogs of orders in the services sector likely grew again in September as the index increased to 61.9 percent from 61.3 percent. Backlogs of orders have grown for 15 of the past 16 months. Thirteen industries reported higher backlogs in September while three reported a decrease.

The services employment index remained above the neutral 50 percent level, coming in at 53.0 percent in September, down from 53.7 percent in August (see bottom of first chart). Fourteen industries reported growth in employment while three reported a reduction. A tight labor market and lack of candidates is likely restraining the employment index.

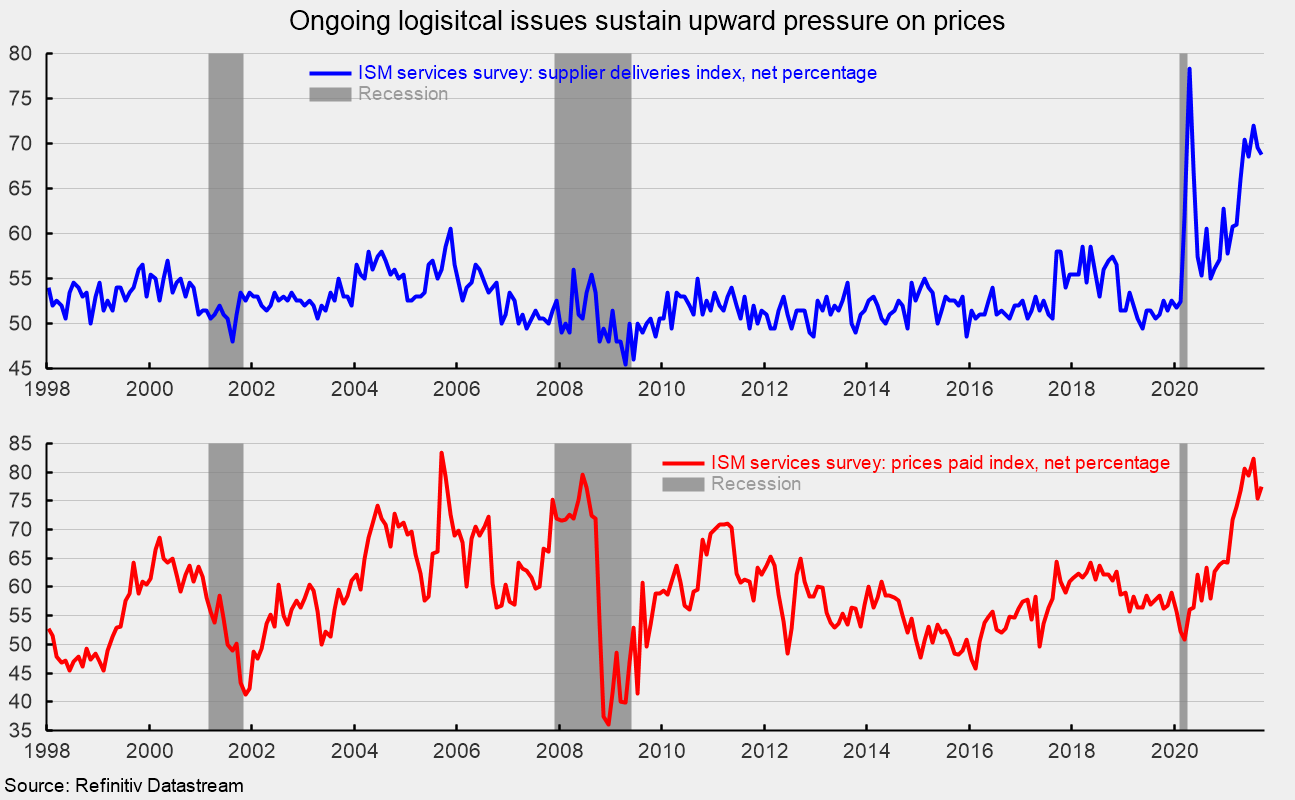

Supplier deliveries, a measure of delivery times for suppliers to nonmanufacturers, came in at 68.8 percent, down from 69.6 percent in the prior month (see top of second chart). It suggests suppliers are falling further behind in delivering supplies to services businesses, but the slippage has decelerated from the prior month. Still, the index remains at a very high level. The slower deliveries are a result of labor constraints, production difficulties including materials shortages, and transportation problems. Seventeen industries reported slower deliveries in September while none reported faster deliveries.

The prices index continues to reflect labor and logistical issues that are restraining supply as demand surges following the easing of government lockdown restrictions. The prices paid index rose to 77.5 percent, up from 75.4 percent in August (see bottom of second chart). Seventeen industries reported paying higher prices for inputs in September while none reported lower prices.

The September report from the Institute of Supply Management suggests that the services sector and the broader economy expanded for the 16th consecutive month in September. Respondents to the survey continue to highlight robust levels of activity and strong demand but also sustained price pressures, materials shortages, particularly related to supply chain, logistics, and transportation issues, and challenges hiring and retaining workers.

Related Posts

Operation Chokepoint 2.0: The Crypto Crackdown Explained (Video)

In this episode of Liberty Curious, Kate Wand discusses the Obama-era Operation Chokepoint, and today’s “Operation Chokepoint 2.0” with AIER Senior Research Faculty Thomas Hogan. Tom explains how government regulators […]

Earth Day, Waste and Productive Complements

It has been just over half a century since the first Earth Day in 1970. Over that time, April 22 has turned into a day with lots of waste cleanup […]

Focusing Exclusively on “Creating Jobs” Can Do More Harm Than Good

We are constantly bombarded by politicians declaring the importance of “creating jobs” in the economy. We regularly see government initiatives like public works projects, “stimulus” programs, and government subsidies enacted […]