Total housing starts rose to a 1.793 million annual rate in March from a 1.788 million pace in February, a 0.3 percent increase. From a year ago, total starts are up 3.9 percent. Total housing permits also rose in March, posting a 0.4 percent gain to 1.873 million versus 1.865 million in February. Total permits are up 6.7 percent from the March 2021 level. Both categories were led by multifamily housing.

Starts in the dominant single-family segment posted a rate of 1.200 million in March versus 1.221 million in February, a drop of 1.7 percent and are off 4.4 percent from a year ago (see first chart). Single-family permits fell 4.8 percent to 1.147 million versus 1.205 million in February (see first chart).

Starts of multifamily structures with five or more units increased 7.5 percent to 574,000 and are up 28.1 percent over the past year while starts for the two- to four-family-unit segment fell 42.4 percent to a 19,000-unit pace versus 33,000 in February. Combined, multifamily starts were up 4.6 percent to 593,000 in March and show a gain of 26.2 percent from a year ago (see first chart).

Multifamily permits for the 5-or-more group jumped 10.9 percent to 672,000 while permits for the two-to-four-unit category were unchanged at 54,000. Combined, multifamily permits were 726,000, up 10.0 percent for the month and up 29.4 percent from a year ago (see first chart).

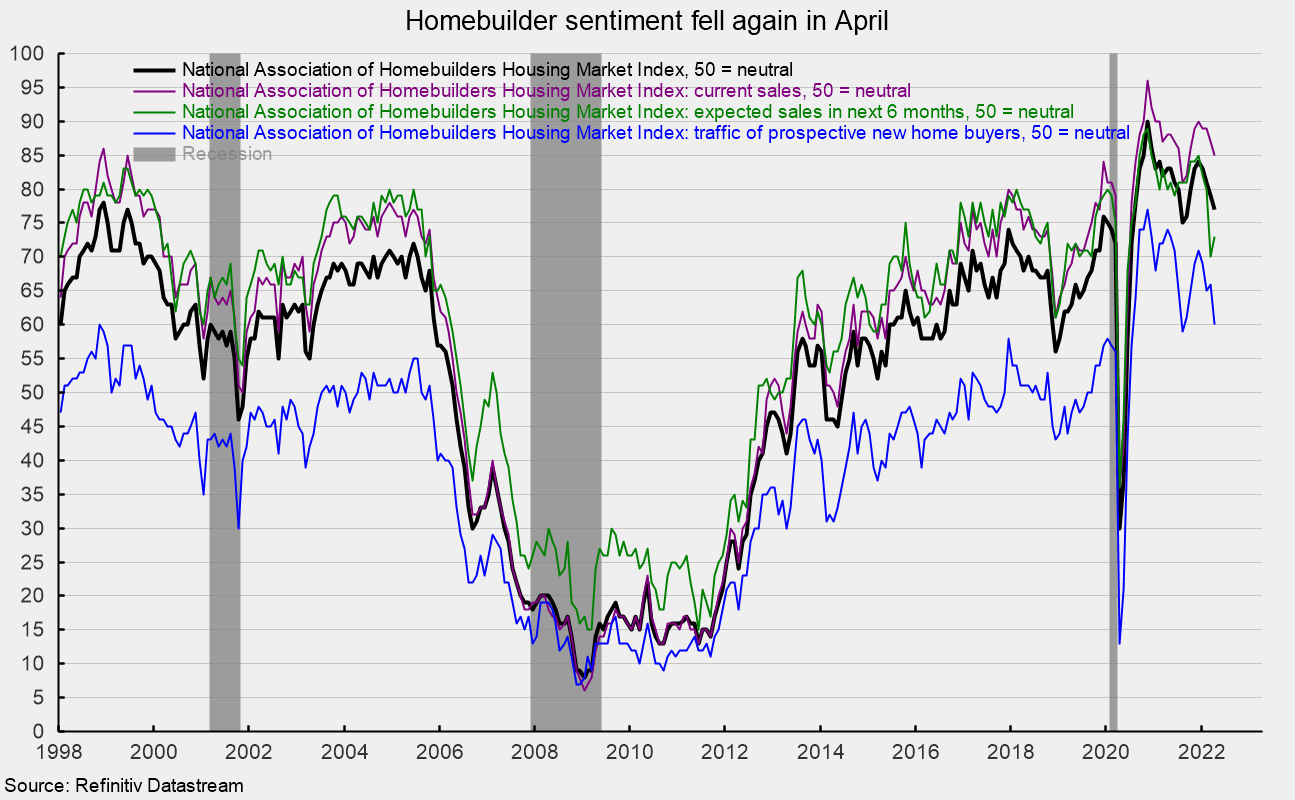

Meanwhile, the National Association of Home Builders’ Housing Market Index, a measure of homebuilder sentiment, fell again in April, coming in at 77 versus 79 in March, but still at a somewhat favorable level. Overall sentiment remains positive, but rising mortgage rates, elevated home prices, and higher input costs are major concerns.

Two of the three components of the Housing Market Index fell in April. The expected single-family sales index rebounded slightly, rising to 73 from 70 in the prior month, but the current single-family sales index was down to 85 from 87 in March while the traffic of prospective buyers index fell six points to 60 (see second chart).

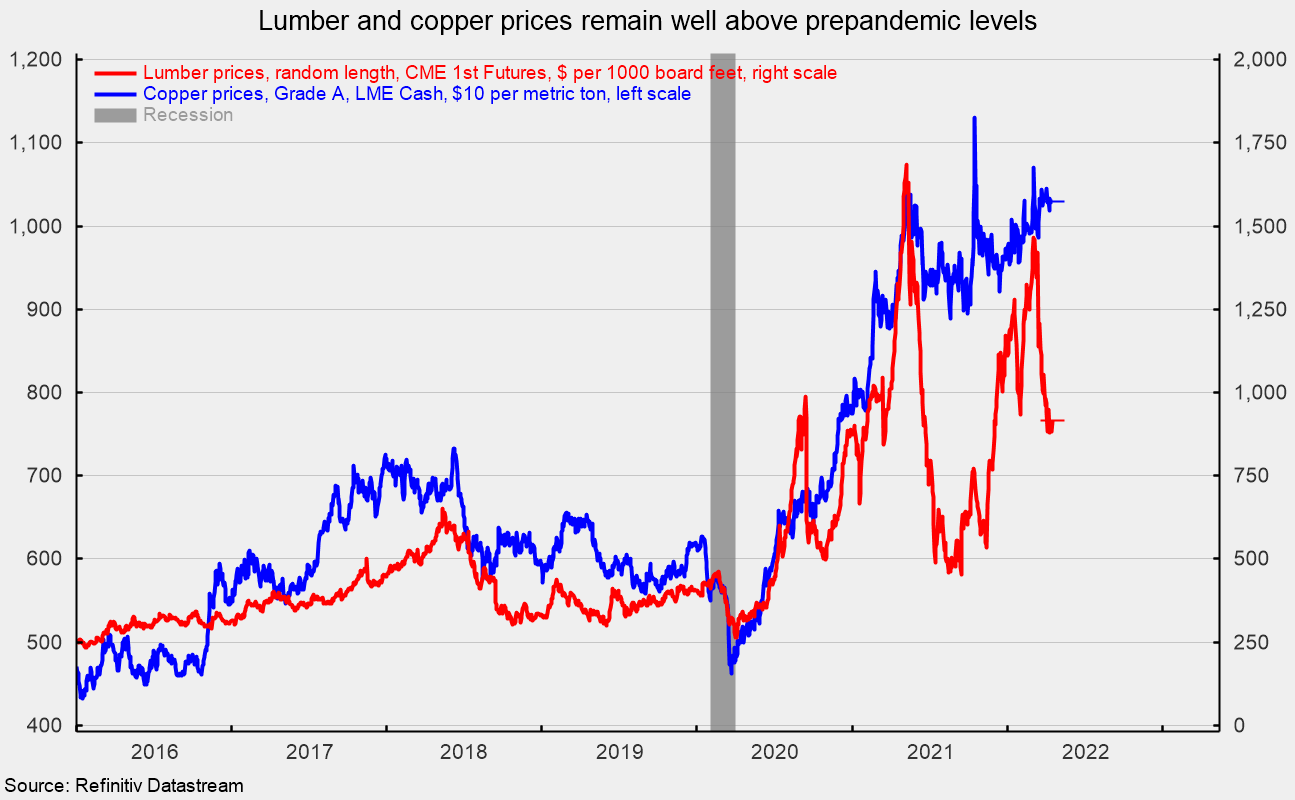

Input costs are a concern for builders, with lumber coming in at around $915 per 1,000 board feet in mid-April, down from peaks around $1,700 in May 2021 and $1,500 in early March 2022 while copper was holding at just over $10,000 per metric ton (see third chart). The high input costs will pressure profits at builders and may lead to more price increases for new homes (see fourth chart).

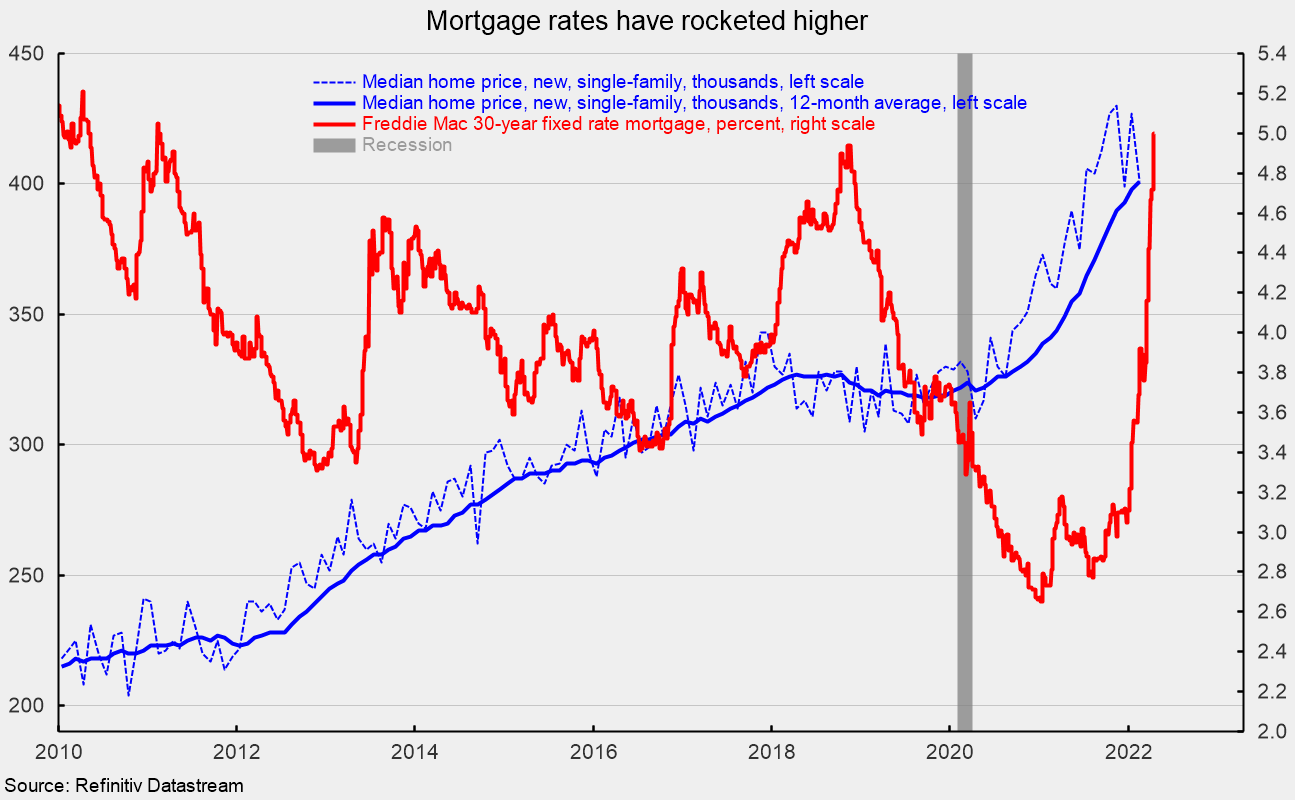

Furthermore, mortgage rates have rocketed higher recently, with the rate on a 30-year fixed rate mortgage coming in at 5.00 percent in mid-April, nearly double the lows in early 2021 (see fourth chart). Higher home prices and higher mortgage rates are likely to be significant headwinds for future housing activity.

After a pullback in activity in the first three quarters of 2021, single-family activity has shown renewed strength. While the implementation of permanent remote working arrangements for some employees may be providing continued support for housing demand, ongoing home price increases combined with the recent surge in mortgage rates will likely work to cool activity in coming months. Threats to future demand combined with elevated input costs are weighing on homebuilder sentiment. The outlook for housing is becoming more guarded.

Related Posts

Operation Chokepoint 2.0: The Crypto Crackdown Explained (Video)

In this episode of Liberty Curious, Kate Wand discusses the Obama-era Operation Chokepoint, and today’s “Operation Chokepoint 2.0” with AIER Senior Research Faculty Thomas Hogan. Tom explains how government regulators […]

Earth Day, Waste and Productive Complements

It has been just over half a century since the first Earth Day in 1970. Over that time, April 22 has turned into a day with lots of waste cleanup […]

Focusing Exclusively on “Creating Jobs” Can Do More Harm Than Good

We are constantly bombarded by politicians declaring the importance of “creating jobs” in the economy. We regularly see government initiatives like public works projects, “stimulus” programs, and government subsidies enacted […]