The Consumer Confidence Index from The Conference Board fell again in June, the second drop in a row and seventh in the last twelve months. The composite index decreased 4.5 points or 4.4 percent to 98.7, the lowest level since February 2021 (see top of first chart). From a year ago, the index is down 23.4 percent. The decline was concentrated in consumer’s expectations for the future.

The expectations component sank 7.3 points, or 9.9 percent, to 66.4 (see middle of first chart) while the present-situation component – one of AIER’s Roughly Coincident Indicators – fell just 0.3 points to 147.1 (see bottom of first chart). The expectations index is down 38.8 percent from a year ago and is at its lowest level since March 2013. The index is below the readings just before the start of three of the last four recessions.

Within the expectations index, all three components fell versus May. The index for expectations for higher income fell 2.0 points to 15.9 while the index for expectations for lower income rose 0.7 points, leaving the net (expected higher income – expected lower income) down 2.7 points to 0.7.

The index for expectations for better business conditions fell 1.7 points to 14.7 while the index for expected worse conditions rose 3.1 points, leaving the net (expected business conditions better – expected business conditions worse) down 4.8 points to -14.8.

The outlook for the jobs market weakened in June as the expectations for more jobs index fell 1.2 points to 16.3 while the expectations for fewer jobs index rose by 2.5 points to 22.0, putting the net down 3.7 points to -5.7.

For the present situation index components, current business conditions and employment conditions weakened slightly. The net reading for current business conditions (current business conditions good – current business conditions bad) was -3.4 in June, down from -1.9 in May. Current views for the labor market saw the jobs hard to get index decrease, falling 0.8 points to 11.6 as the jobs plentiful index fell 0.6 points to a still-strong 51.3 resulting in a 0.2-point gain in the net to 39.7. A net above 40 is considered strong by historical comparison.

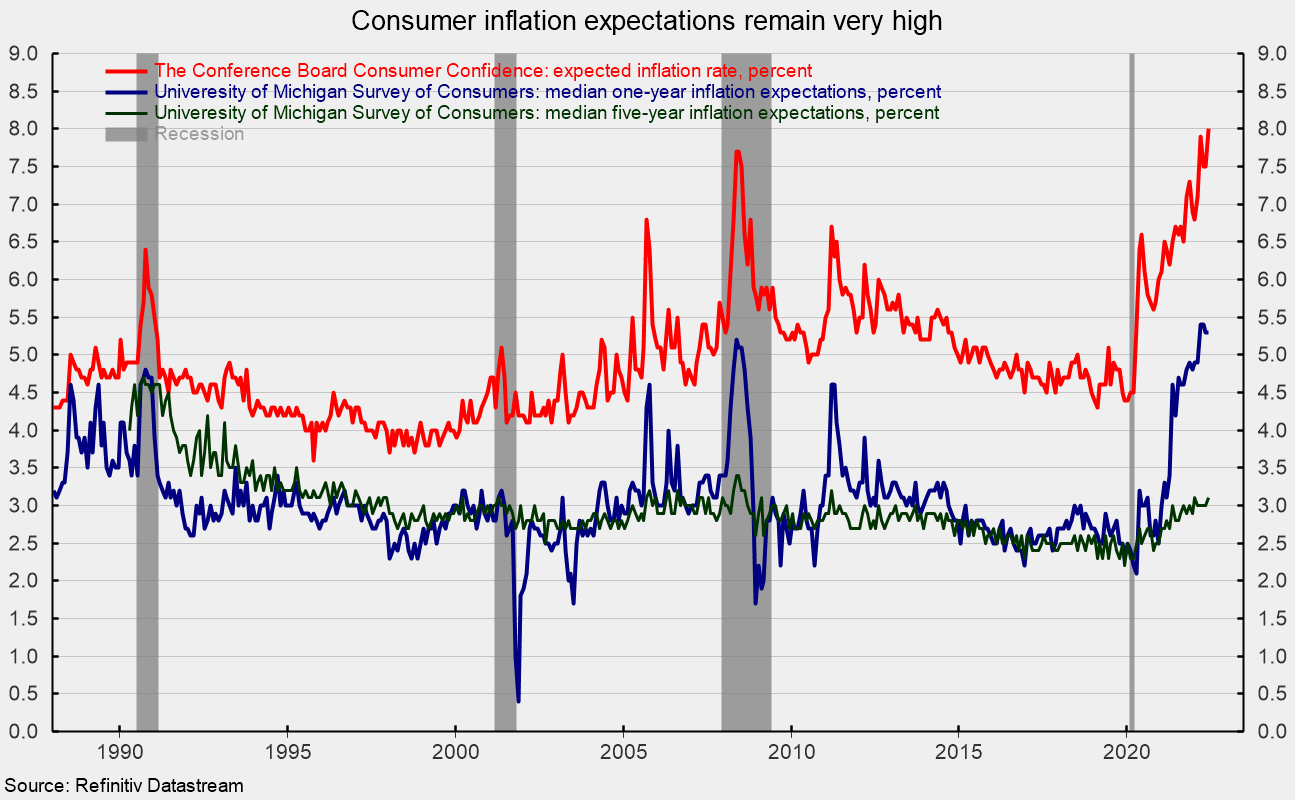

Inflation expectations rose to 8.0 percent in June, a record high; expectations were 4.4 percent in January 2020 (see second chart). The sharp rise in expected inflation from The Conference Board survey is consistent with the University of Michigan survey results, though the magnitudes are different (see second chart). Inflation expectations remain extremely high as prices for many goods and services continue to rise at an elevated pace. The extreme outlook for inflation is a key driver of weaker expectations among consumers.

The surge in prices for many consumer goods and services is largely a function of shortages of materials, a tight labor market, and logistical issues that prevent supply from meeting a post-lockdown-recession surge in demand, though there has been significant progress boosting production. Price pressures have been compounded by surging energy prices as a result of the Russian invasion of Ukraine and periodic lockdowns in China. Furthermore, the intensifying Fed tightening cycle raises the risk of a policy mistake and adds to the extreme level of risk and uncertainty in the overall economic outlook.

Related Posts

Operation Chokepoint 2.0: The Crypto Crackdown Explained (Video)

In this episode of Liberty Curious, Kate Wand discusses the Obama-era Operation Chokepoint, and today’s “Operation Chokepoint 2.0” with AIER Senior Research Faculty Thomas Hogan. Tom explains how government regulators […]

Earth Day, Waste and Productive Complements

It has been just over half a century since the first Earth Day in 1970. Over that time, April 22 has turned into a day with lots of waste cleanup […]

Focusing Exclusively on “Creating Jobs” Can Do More Harm Than Good

We are constantly bombarded by politicians declaring the importance of “creating jobs” in the economy. We regularly see government initiatives like public works projects, “stimulus” programs, and government subsidies enacted […]