We have been living under an illusion that the relationship between nominal GDP and the quantity of circulating currency is dead. This illusion began in 2008, when the Federal Reserve began expanding the value of its assets without expanding the value of circulating currency. Instead, banks were paid to hold this newly created money on account at the Federal Reserve. The newly created money, thus, did not generate inflation despite expectations among many that high inflation was imminent.

In the long run, inflation is determined by the rate of expansion of circulating currency and growth in real productivity. Real productivity growth is deflationary, but tends to be modest and relatively stable. Thus, the growth rate of circulating currency tends to be correlated with the growth rate of total expenditures, as well as inflation.

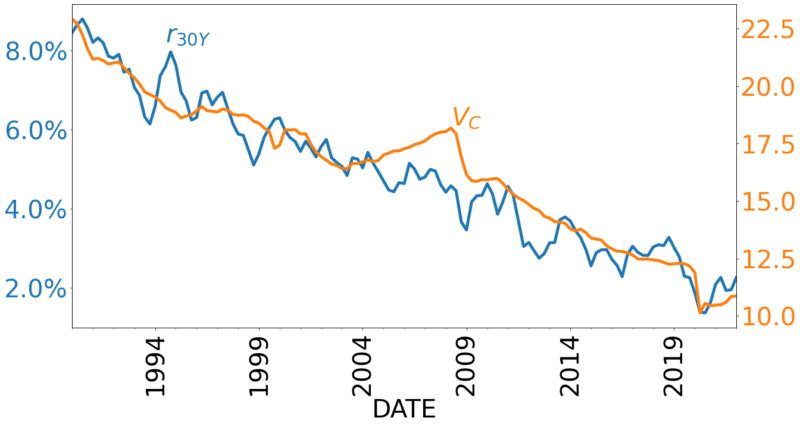

After the 2008 Financial Crisis, the rate of inflation hovered around 1.7 percent. From the end of that crisis until recently, the velocity of currency trended downward modestly, mirroring the fall in long-term nominal interest rates. Figure 1 conveys this relationship between velocity of currency (right axis) and the nominal interest rate paid on 30-year US Treasuries (left axis).

It is true that an increase in the quantity of money will support a proportional increase in the level of expenditures, as long as the velocity of currency is stable. A more sophisticated expression of this truth holds that the velocity of currency is stable with respect to interest rates. Over the last several decades, the velocity of money currency has tended to follow the downward trend in interest rates. Although the relationship has not been 1-to-1, expansion of the stock of currency has tended to positively impact the level of total expenditures and the price level. For much of this period, the stock of circulating currency grew at a rate of about 7 percent while the rate of growth of nominal GDP was often in the range of between 3 percent and 5 percent.

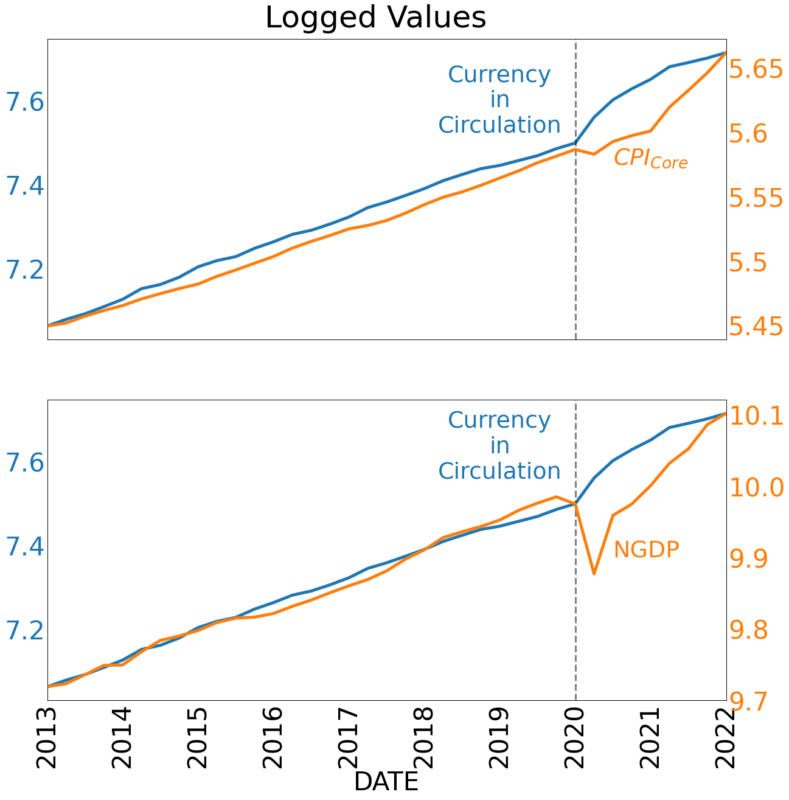

In accordance with this logic, the FOMC has responded to increasing inflationary pressure by reducing the growth rate of currency in circulation as the level of nominal GDP has broken above the pre-2020 trend. In the meantime, however, the balance sheet continued to expand into the first quarter of 2022. This recent correlation between balance sheet expansion and the annual rate of inflation has led many to believe that the Fed’s current stance is too easy. The balance sheet increased for much of the previous decade without generating significant inflation. Circulating currency serves as reserves that support lending within the financial system. Policymakers and protocols governing monetary policy – for example, the Overnight Reverse Repurchase Agreement Facility – have supported stability in the level of currency in circulation. Stability in the path of NGDP tends to reflect stability in the path of circulating currency. Not coincidentally, the jump in the path of currency in circulation that began in the first quarter of 2020 has been followed by a similar jump in NGDP and in CPI (vertical line indicates start of first quarter of 2020). Those who would like to predict the future path of nominal GDP and of the price level should focus on currency in circulation, not the size of the balance sheet.

Inflation, Balance Sheet Expansion, and Fed Solvency

Claims linking inflation to the size of the balance sheet may stem, in part, from focus by Fed officials on the size of the balance sheet in recent months. Recent statements by Fed officials reflect that higher inflation readings have made these policymakers increasingly concerned about the size of the balance sheet.

Absent a solvency crisis, however, a larger balance sheet is most likely to be associated with lower interest rates and lower rates of real income growth. This program of balance sheet expansion, called quantitative easing, influences resource allocations by asset class and maturity length. While some might hope that quantitative easing stimulates aggregate demand, there is little empirical evidence or theory to suggest that it does. Since the Federal Reserve began expanding the balance sheet greatly in excess of circulating currency, the rate of real GDP growth has fallen to historic lows. For much of this period, the level of GDP was below its potential path. And as the Fed began balance sheet reductions in 2017, these reductions were accompanied by relatively higher rates of real GDP growth. In the least, it is unlikely that quantitative easing supports expansion of aggregate demand.

Quantitative easing certainly impacts resource allocations. The Fed’s acquisition of subprime mortgages during the 2008 Crisis lowered the risk of financial insolvency for firms that would have been left holding these mortgages. This was intended to help stabilize a housing market that was in meltdown and seems to have helped that market weather the liquidity crisis. Along with purchases of long-term US Treasuries, this policy was also intended to lower interest rates at the upper end of the yield curve. The most noteworthy effect of quantitative easing, then, has been to allocate credit toward particular classes of borrowers.

While balance sheet expansion has not been the cause of inflation over the last decade, this does not mean that the Federal Reserve can expand the balance sheet without limit. Balance sheet expansion absent expansion of circulating currency is not inflationary so long as there is not a mismatch between the assets and liabilities sides of the balance sheet. Assets yield income. On the other hand, much of the liabilities side of the Fed’s balance sheet implies income payments that must be made by the Fed in order to maintain solvency. As long as the income earned by the Federal Reserve exceeds expenditures, the Fed remains solvent.

Expansion of the Federal Reserve’s balance sheet simultaneously increases interest-earning assets and liabilities that require interest payments from the Fed. The Federal Reserve prevents inflation by simultaneously borrowing the funds that it uses to pay for assets purchased. For example, the Federal Reserve may credit interest-bearing deposit accounts or may borrow funds at interest from the overnight lending market in order to offset currency created via its purchase of assets.

Monetary stability requires that the interest payments from the Federal Reserve are provided from the receipts adding to its income rather than from money creation. That is, Federal Reserve profits need to remain positive. Positive profits, defined by income above operating expenses, are remitted to the US Treasury. Negative profits either must be paid by the US Treasury or must be covered by the creation of new money. Negative profits would likely hurt investor confidence.

The assets side of the balance sheet is supposed to constrain the liabilities side. Insolvency occurs when the value of liabilities are not offset by the value of assets. Insolvency could occur, for example, due to rising interest rates. Suppose that investors lose faith in the ability of the Federal Reserve to maintain low and stable inflation. Rising mortgage rates would devalue mortgage-backed securities already held by the Fed that comprise a significant portion of the Fed’s assets. Thus, as interest rates rise, the Federal Reserve will likely need to begin reducing the size of the balance sheet in order to 1) reduce losses on the assets side of its balance sheet and 2) to reduce interest payments that it owes to institutions and investors. As long as the Federal Reserve remains solvent and investors expect that it will remain solvent, a large balance sheet cannot, on its own, be the cause of inflation.

At present, there seems to be little reason to doubt the ability of the Federal Reserve to remain solvent as even doves like Lael Brainard, who was recently confirmed as Vice Chairwoman, are calling for aggressive tightening.

Will Inflation Continue to Rise?

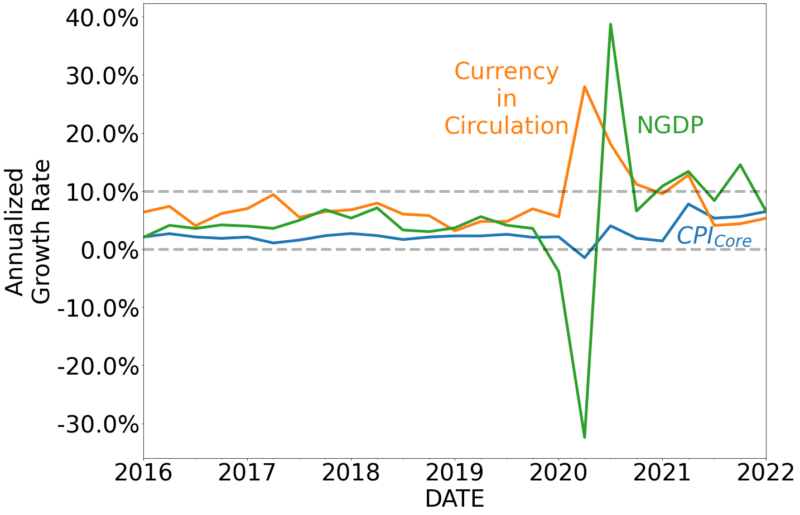

As the year-over-year rate of inflation has increased, many commentators have begun to reflect on the relationship between easy money and inflation. However, few of these commentators have been consistently correct in their evaluation of Fed policy. Most do not differentiate between an increase in the Fed’s balance sheet and expansion of currency in circulation. Over the last year, year-over-year rates of inflation have been rising as a result of the increasing rate of expansion of circulating currency orchestrated by the Federal Reserve during 2020. The good news is that annualized monthly and quarterly rates of inflation have been stable over the last year. The Federal Reserve began moderating this expansion of currency in circulation in the last year as nominal GDP returned to its pre-crisis trend. Nominal GDP has overshot this trend, which is why we have been experiencing relatively high rates of inflation. But there is reason to expect that this overshoot is currently somewhere close to its greatest extent.

If excessive increases in inflation and the growth rate of nominal expenditures are caused by excessive increases in the growth rate of circulating currency, then we should expect inflation to ease in the near future as the rate of expansion of currency in circulation has moderated.

The swift expansion of circulating currency by the Federal Reserve helped expenditures to bounce back immediately after plunging in the second quarter of 2020. The growth rate of currency in circulation has been back to pre-crisis rates for at least 2 quarters. We should expect inflation and the growth rate of expenditures to follow and inflationary winds to subside as a result.

Related Posts

Operation Chokepoint 2.0: The Crypto Crackdown Explained (Video)

In this episode of Liberty Curious, Kate Wand discusses the Obama-era Operation Chokepoint, and today’s “Operation Chokepoint 2.0” with AIER Senior Research Faculty Thomas Hogan. Tom explains how government regulators […]

Earth Day, Waste and Productive Complements

It has been just over half a century since the first Earth Day in 1970. Over that time, April 22 has turned into a day with lots of waste cleanup […]

Focusing Exclusively on “Creating Jobs” Can Do More Harm Than Good

We are constantly bombarded by politicians declaring the importance of “creating jobs” in the economy. We regularly see government initiatives like public works projects, “stimulus” programs, and government subsidies enacted […]