While the US Federal Reserve is making significant efforts to prevent the money market rate from falling below zero with the help of so-called reverse repurchase agreements, negative interest rates are appearing in a number of the euro area’s financial markets. Why is this happening? And what does it mean for wealth and prosperity in the euro area?

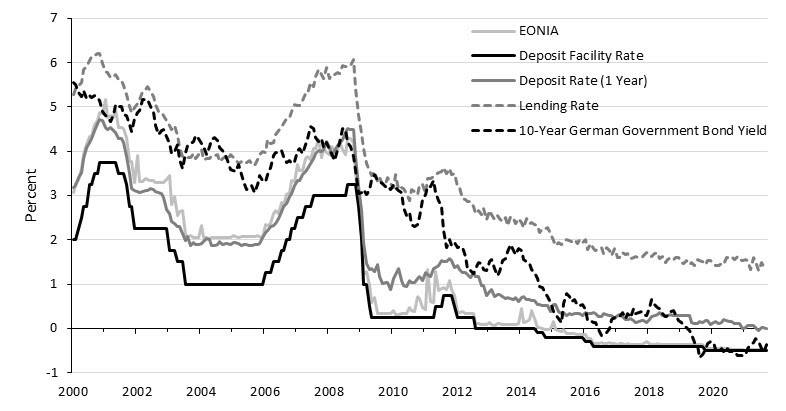

The starting point was marked by the interest rate charged by the European Central Bank on commercial banks’ deposits on their accounts with the ECB, the so-called deposit facility rate. Since the outbreak of the European financial and debt crisis, the ECB engaged in extensive purchases of government and corporate bonds, which inflated the commercial banks’ deposits with the ECB. The deposits of the commercial banks with the ECB by far exceed the minimum reserve requirements and keep rising. In June 2014, the interest rate on the ECB’s deposit facility, which serves as an interest rate floor, was set for the first time in negative territory at -0.1% and was reduced to -0.5% since then (Figure 1).

This has led to pressure on commercial banks to pass on the negative interest rates to the deposits of households, companies, and municipalities. The reason is that since 2008, the ECB’s persistent low, zero and negative interest rate policies have put pressure on commercial banks’ interest margins, interest surpluses, and thereby profits. Since 2014, euro area banks have paid around €45 billion in penalty interest to the ECB. While initially only depositors with high amounts of savings were affected, negative interest rates are increasingly passed on to savers with smaller amounts of savings. In many cases where this was not legally possible, the negative interest took the form of so-called “custody fees,” with bank fees increasing.

Figure 1: Interest Rates in Germany

The interest rate on the European interbank market (EONIA) closely follows the deposit facility rate, and therefore has also turned negative (Figure 1). The interbank rate is charged when banks lend to each other over short periods of time to offset liquidity shortages or surpluses. In the past, interest had to be paid on such short-term loans. Now, because the ECB has flooded commercial banks with liquidity through its extensive asset purchase programs, and interest has to be paid for holding reserves at the ECB, commercial banks are only willing to accept liquidity from other banks in return for compensation.

Interest rates on some government bonds in the euro area became negative because the ECB stepped up its purchases of government bonds. At the height of the European debt crisis in July 2012, ECB President Draghi (ECB 2012) signaled that the ECB was committed to saving the euro by buying government bonds (“whatever it takes”). If the volume of the ECB’s government bond purchases is based on what is needed to prevent a sovereign default of southern euro area countries such as Italy and Greece, and if the purchases of government bonds of individual euro area countries are made in proportion to the ECB’s capital key, then the interest rates of euro area countries with comparatively low default risk can fall into negative territory. This has been the case for 10-year German government bonds since April 2019 (Figure 1). The government bonds of Austria, Finland and the Netherlands currently also have negative yields.

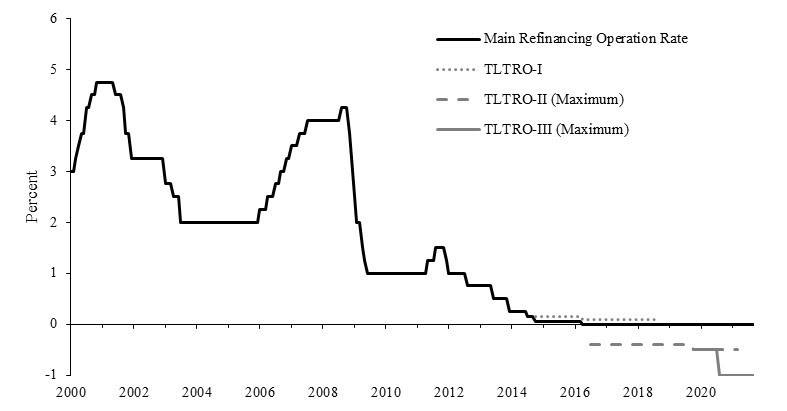

Finally, the ECB introduced a negative interest rate on the so-called Targeted Longer-Term Refinancing Operations (TLTROs) (Schnabl and Sonnenberg 2020). Until 2015, commercial banks still had to pay interest for refinancing at the ECB (Figure 2). Yet since then, the interest rate on TLTRO-II and TLTRO-III loans is negative, currently between -0.5% to -1%. This implies that banks have an incentive to extend more loans to enterprises, thereby reducing their financing costs.

Figure 2: Interest Rates on Eurosystem Refinancing Operations

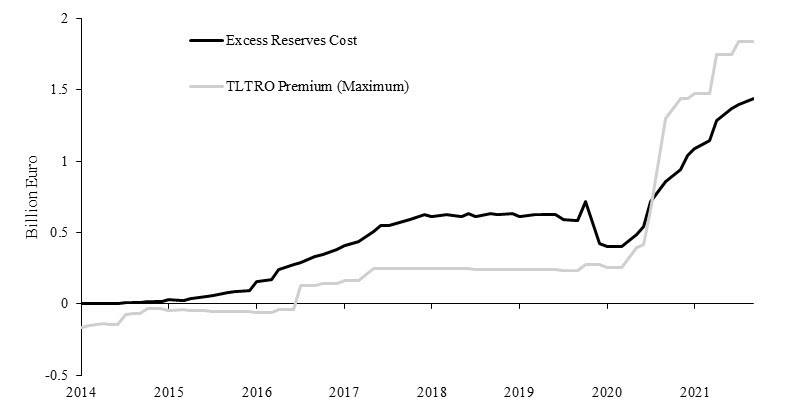

The upshot is that “penalty interest rates” on commercial banks’ reserve holdings at the ECB are (partially) offset or even overcompensated by “bonus interest rates” for borrowing from the ECB under certain conditions. If TLTRO-III loans bear an interest rate of -1%, from the perspective of the euro area banking sector as a whole, the “bonus interest rates” (premium) have been higher than the “penalty interest rates” since 2020 (Figure 3). Yet banks are affected in different ways. The net effect is positive for Italian and Spanish banks, whereas it is negative for German banks. In general, the ECB seems to work with carrots and sticks: First, the profitability of banks is weakened by negative interest rates on the deposit facility. Then, a positive interest rate is granted for taking credit from the ECB, if certain conditions are fulfilled.

The upshot is that the ECB has turned the euro area capital market upside down. In the old world, the Deutsche Bundesbank and other European central banks set the key interest rate in positive territory. Commercial banks financed investment projects that generated a higher return than their positive lending rates. Alternatively, commercial banks held government bonds on which they received a positive interest rate. The resulting interest surpluses allowed banks to cover their costs and pay interest to savers on their deposits. The returns generated by enterprises via investment were thus divided between entrepreneurs, banks and households (savers).

Figure 3: Monthly Income and Expenses of the Eurosystem Due to Negative Interest Rates

In the ECB’s brave new credit world, the ECB sets interest rates on deposits in negative territory, while companies receive a (kind of) subsidy for their investments. However, as resources are scarce and expected returns on investment are now only of limited concern for lending, there must be alternative criteria for credit allocation. The European Commission is already working on plans to channel savings in the EU into green investments (European Commission 2021a), based on the climate-friendly classification of individual investment projects (taxonomy) (European Commission 2021b). The ECB strongly signals support for greening the financial sector (Lagarde 2021). Initial ECB climate stress tests of banks indicate that different loans could be assigned different “support” by the ECB depending on the “climate classification.”

This means not only much more power for the ECB, but also drastic welfare losses. If the allocation of capital is no longer based on the criterion of economic efficiency, but on the assessment of bureaucrats on climate friendliness, this corresponds to a system change from a market economy to a (green) planned economy. The consequence might be a large misallocation of funds and waste of resources. The associated loss of wealth is likely to be reflected in negative real growth rates as well as declining real wages. The widely negative real interest rates, which have already been a reality in some segments of the European capital markets, might foreshadow this loss of welfare for the European people.

Related Posts

Operation Chokepoint 2.0: The Crypto Crackdown Explained (Video)

In this episode of Liberty Curious, Kate Wand discusses the Obama-era Operation Chokepoint, and today’s “Operation Chokepoint 2.0” with AIER Senior Research Faculty Thomas Hogan. Tom explains how government regulators […]

Earth Day, Waste and Productive Complements

It has been just over half a century since the first Earth Day in 1970. Over that time, April 22 has turned into a day with lots of waste cleanup […]

Focusing Exclusively on “Creating Jobs” Can Do More Harm Than Good

We are constantly bombarded by politicians declaring the importance of “creating jobs” in the economy. We regularly see government initiatives like public works projects, “stimulus” programs, and government subsidies enacted […]