In June, the Federal Open Market Committee (FOMC) raised the federal funds rate target by 75 basis points, moving the target range to 1.5-1.75 percent. This was the biggest single increase in the federal funds rate target since 1994. Why has the Fed so quickly shifted its stance? And how are investors responding to this financial tightening?

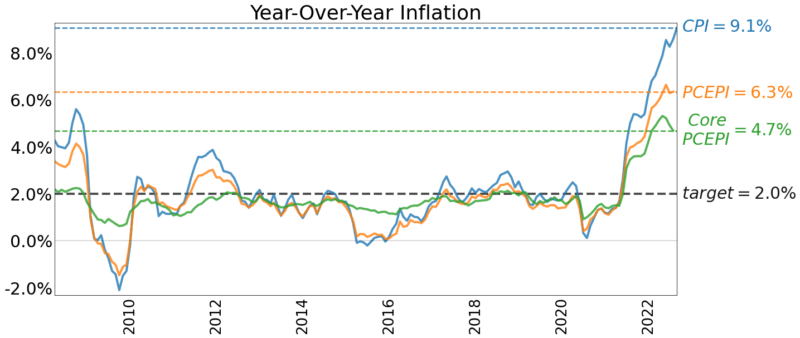

As noted in the Federal Reserve’s Statement on Longer-Run Goals and Monetary Policy Strategy, the FOMC “seeks to achieve inflation that averages 2 percent over time” as measured by the personal consumption expenditures price index (PCEPI ). PCEPI inflation is measured using a price level that weights prices in light of consumer expenditures. The Fed also monitors Core PCEPI inflation, which excludes food and energy, since this measure tends to be a better predictor of the PCEPI over longer periods of time.

Some complain when the Fed officials or economists refer to Core PCEPI, on the grounds that food and energy prices matter a lot to American consumers . But such complaints are misguided. The Federal Reserve does not deny the importance of food and energy prices, which are included in the PCEPI it targets. The attention paid to Core PCEPI (and other variables) is merely intended to reduce the odds that the Fed overreacts to short term swings in food and energy prices, which lead PCEPI inflation to fluctuate around Core PCEPI inflation.

Year-over-year Core PCE inflation has been trending downward over the last few months. It reached a high of 5.3 percent in February. In May, it was just 4.7 percent.

PCEPI inflation, in contrast, has surged. Higher energy prices, which are largely due to Russia’s invasion of Ukraine and the corresponding economic sanctions, have lifted gas prices to new highs. In many states, the price of gas is higher than $5.00 per gallon, with the price of diesel often pushing above $6.00 per gallon. This has played a role in lifting PCEPI and CPI inflation.

The more important effect of higher energy prices is their constraint they put on economic growth. At the moment, the FOMC wants to prevent a significant takeoff in PCEPI inflation. Aggressive policy will slow inflationary pressure in general and likely bring rates down.

The Future of Inflation

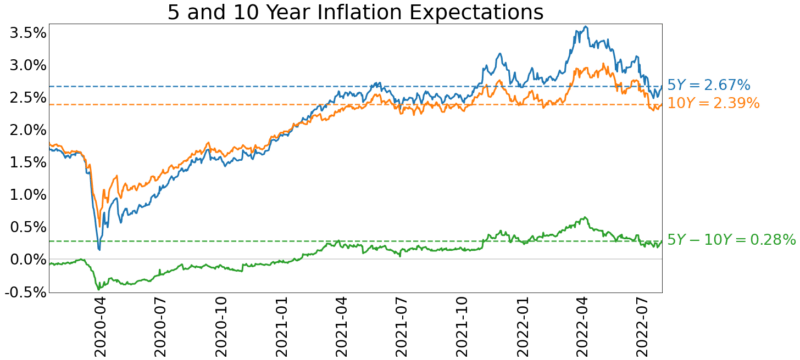

What are the markets saying about expected inflation? One way to distinguish between short-run and long-run inflation expectations is to compare the 5- and 10-year breakeven rates of inflation. The breakeven inflation rate compares the rate of return on inflation-compensated bonds to rates on uncompensated U.S. Treasuries of the same maturity length. They subtract the rate on inflation-adjusted securities from non-adjusted securities. Since these Inflation Protected Securities adjust for inflation as measured by the CPI, the breakeven inflation rates refer to expected changes in CPI.

We can compare the spread on 5-year bonds to 10-year bonds in order to provide a clearer picture of the inflation expectations over time. A wider spread between the 5- and 10-year breakeven rates means that there exists a discrepancy between short- and long-run inflation expectations.

In the plot, I indicate the spread between these two by subtracting the 10-year breakeven rate from the 5-year breakeven rate. When the 5-year breakeven rate is higher than the 10-year breakeven rate, this means that investors expect that inflation in the near future will be higher on average than in the more distant future. The greater the spread between the rates, the greater the discrepancy between short-run and long-run inflation expectations.

In the first quarter of 2021, short-term inflation expectations rose above longer-term inflation expectations. Investors signaled great concern in April, as the gap between 5- and 10-year breakeven inflation reached 0.65 percent. Since that time, Fed Chair Jerome Powell and other members of the FOMC have voiced their concerns about controlling inflation and inflation expectations. The return of the gap to 0.28 percent indicates that investors are convinced that the Fed is serious about tightening and will be effective. With the change in stance, investors expect that inflation will not only be lower on average over the next 5 to 10 years, but that there will be a smaller discrepancy between inflation in the short- and long-run.

Inflation Expectations and the Pace of Interest Rate Increases

Jerome Powell is slamming on the breaks. But how long and how much should we expect Powell’s Fed to tighten? It is difficult to predict the path of policy precisely, but it seems clear that Powell intends to continue raising the federal funds rate target until inflation expectations have cooled. In recent months, inflation expectations have followed a downward trend alongside Core PCEPI inflation. The cooling of inflation expectations is encouraging news since these expectations refer to the more volatile and higher CPI. But PCEPI inflation has continued to rise.

Powell’s Fed has made clear that its 2 percent inflation target is not a symmetric target, meaning that it will not compensate for long periods where inflation is above 2 percent. That means it is an average inflation target with upward bias. Still, current inflation expectations are above 2 percent. If Powell and the FOMC want the target to be effective, they must convince investors that the Fed will take action required to keep PCEPI at 2 percent. And they must do so swiftly. The longer inflation is above 2 percent , the less credible will be the Fed’s commitment to maintain the 2 percent target. And since the target is not a true average target, the best the Fed can do to maintain stable inflation expectations is to swiftly move PCEPI inflation to 2 percent.

This is one reason to think that the FOMC may “overtighten”. Prioritizing a soft landing over maintenance of the 2 percent target would cause a divergence between inflation expectations and the inflation target. The slower the FOMC moves to lower the rate of inflation when it is greatly elevated—it is currently more than 2 percentage points above target—the more markets will perceive the 2 percent target as an ineffective constraint. The result will be relatively higher inflation expectations and interest rates in the long-run, and a persistent discrepancy between the stated inflation target and inflation expectations. To avoid this, the Federal Reserve might prioritize lower inflation in the short-run.

The quiet shift from a symmetric to asymmetric 2-percent target undermines the Fed’s credibility. It says it intends to deliver 2 percent inflation on average, but its asymmetric approach means that inflation will tend to be greater than 2 percent on average. If the FOMC thinks inflation should be higher than 2 percent on average, it should adopt a higher inflation target—say, 3 percent—and compensate for periods of excess inflation by also promoting inflation rates below the average target for extended periods. Doing so would stabilize inflation expectations and increase the likelihood of a soft landing, without necessitating a swift tightening intended to signal that the Fed is serious.

Related Posts

Operation Chokepoint 2.0: The Crypto Crackdown Explained (Video)

In this episode of Liberty Curious, Kate Wand discusses the Obama-era Operation Chokepoint, and today’s “Operation Chokepoint 2.0” with AIER Senior Research Faculty Thomas Hogan. Tom explains how government regulators […]

Earth Day, Waste and Productive Complements

It has been just over half a century since the first Earth Day in 1970. Over that time, April 22 has turned into a day with lots of waste cleanup […]

Focusing Exclusively on “Creating Jobs” Can Do More Harm Than Good

We are constantly bombarded by politicians declaring the importance of “creating jobs” in the economy. We regularly see government initiatives like public works projects, “stimulus” programs, and government subsidies enacted […]