As inflation hits fiat currencies, a new idea is emerging in the cryptocurrency ecosystem. “Flatcoins,” or stablecoins tied to the cost of living rather than fiat currencies, are currently being tested as an attempt to provide more price stability than fiat-pegged alternatives.

Stablecoins, or cryptocurrencies mimicking the value of another currency like the dollar or the euro, have grown in popularity in recent years. They offer users an onramp, connecting mainstream finance to the cryptocurrency ecosystem. Individuals and institutions purchase stablecoins with their native currency and use them to buy various digital assets.

In addition to their role as an onramp, stablecoins serve an alternative use. Central bank profligacy is causing inflation worldwide, leading many outside the West to protect their wealth in stablecoins tied to assets such as US dollars. For example, in Russia, stablecoin use jumped from 55 percent of total crypto volume last February to 67 percent in March, as ordinary Russians sought to protect their savings via stablecoins.

Although dollars are less inflationary than bolivars or rubles, they are not immune to inflation. As a result, stablecoins tied to fiat currencies are suddenly less stable.

Unlike fiat-collateralized stablecoins, flatcoins are a new variety of stablecoins, which developers seek to tie to maintaining a constant value in purchasing power. And although they represent an interesting bid for stability in today’s environment, flatcoins are not battle-tested and face risks.

Stablecoins: Algorithmic, Collateralized, Flat?

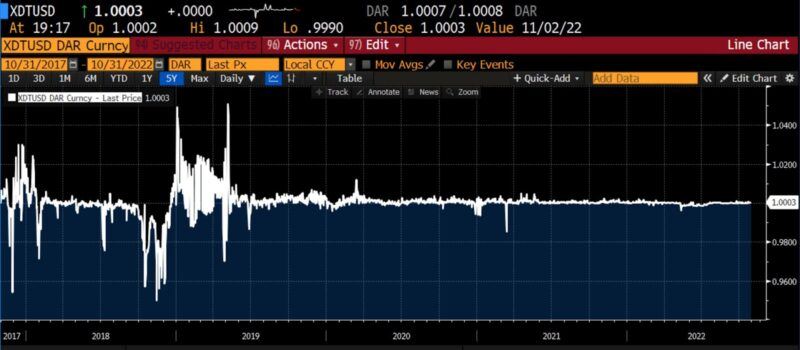

The largest class of stablecoins are fiat-collateralized, such as Tether, Circle, and Binance USD, representing most of the asset classes’ market capitalization. Today, fiat-collateralized stablecoins are considered safe after enduring market tests such as massive redemptions. Tether, for example, redeemed $16 billion worth of Tethers (USDT) in exchange for dollars last spring, with $7 billion of the redemptions occurring in 48 hours.

Tether-USD rate (5 years)

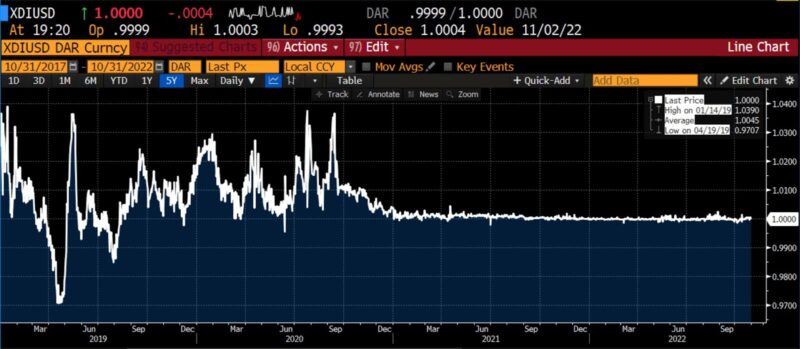

Crypto-collateralized stablecoins such as DAI represent another option. Maker DAO, a decentralized autonomous organization, manages DAI, and every time more DAI is minted, the protocol adds more cryptocurrencies as collateral. Since its inception, DAI has traded at near parity with the US dollar.

DAI-USD rate (2019 – present)

In addition to fiat-collateralized and crypto-collateralized stablecoins, enterprising individuals have attempted to create algorithmic stablecoins, uncollateralized and maintained via pegs, with sparse successes. The most famous attempt at an algorithmic stablecoin, UST, belongs to the recently collapsed Terra/Luna ecosystem. In their report, All Falls Down, Nic Carter and Allen Farrington analyze the collapse in great detail. According to Carter and Farrington:

The chief collateral backing of the UST coin was Luna. As a monetary policy, this is deeply troubling given Luna’s value is mostly derived from the market’s perceptions of the robustness of UST, alongside the perceived vibrancy of the Terra network. On the one hand, one could make the case that the gas token for a layer 1 smart contracting blockchain ought to increase in value with the utility of the ecosystem it supports due to pure supply and demand, and little else. On the other, if you find this worryingly recursive and self-referential, you are not alone.

Luna-USD rate (2021 – present)

Cryptocurrencies and inflation

Rarely since the birth of crypto, has price stability been as immediate a concern as it has been since early 2021. Since that time, in the wake of highly expansionary fiscal and monetary policy measures in response to the pandemic, price levels worldwide began to surge. Central banks delayed their response, largely taking their cues from the Federal Reserve. After officials dismissed the inflationary updraft as “transitory” for some months, it became clear in late 2021 and early 2022 that the rise in prices was widespread and persistent.

While the Fed initiated contractionary policy measures starting in March of 2022, at that point, it had delayed action for at least twelve months. And while the American central bank has responded with aggressive rate hikes, in much of the rest of the world, higher year-over-year inflation has been met more tepidly. Asset prices, including those of cryptocurrencies, have been pummeled as credit has contracted.

Argentina’s national CPI is currently an estimated 83 percent annualized. While not meeting Cagan’s definition of hyperinflation, the upward surge in the price level has pernicious effects, most assuredly hurting citizens. Crypto-savvy Argentinians are using fiat-pegged stablecoins like Tether as a refuge: stablecoins which, ideally, tie the size of the coin float to the units of currency held in some form of depository trust (thus, 1 million stablecoins should be backed by 1 million dollars, euros, or whatever currency they purport to be tied to.) This, of course, is fraught with peril on several levels.

Argentine Peso-US Dollar cross & Argentinian CPI, year-over-year (2017 – present)

First, the problem of transparency: many coin-issuing firms are reluctant to allow audits, and thus the sufficiency of currency (or, as the case may be, other liquid assets) backing the coin float is impossible to verify. Additionally, fiat-backed stablecoins are centralized, and therefore antithetical to the animating spirit of decentralized finance. They are more akin to an old-economy, asset-backed security than a cryptocurrency.

Flatcoins

The concept behind flatcoins is straightforward: if tied to a good or a basket of goods (akin to the Consumer Price Index), over time, the price of the coin will rise to offset inflationary increases, and (one assumes) decreases correspondingly with a deflationary price trend.

Less clear is whether flatcoins will reflect changes in relative prices, or if algorithms can distinguish between price changes driven by changes in supply/demand versus the Friedmanite “more money chasing the same number of goods and services.”

The concept evokes Irving Fisher’s “compensated dollar” plan, proposed in the early part of the twentieth century. By its working:

if an index of the price level should increase by, say, 1 percent, then the purchasing power of a dollar gold-certificate would be restored by increasing the ‘gold content’ of a dollar by 1 percent; and if during the following quarter that should not succeed in restoring the original price level, the gold content would be further increased—and so forth. Here, then, was a rule in the modern sense of the term …. Now, to increase the gold content of the dollar means to decrease the dollar price of a given quantity of gold, and vice versa[.]

Further, there is perpetual chatter about the BRICS (Brazil, Russia, India, China, and South Africa) nations coming together to create a commodity-pegged currency that rivals the US dollar. The Meta (née Facebook) concept of Libra, as well, contemplated a coin collateralized in such a way that:

while approximately half of each Libra coin w[ould] derive half of its value from the US Dollar, Euro denominated bonds [would] have 30 percent stakeholding in the basket of currencies. Euro (18 percent), Yen (14 percent), the British Pound (11 percent) and Singapore dollar (7 percent) [would] make up the rest.

Although the idea is not unique to the world of cryptocurrencies, a privately issued flatcoins offer benefits over those partly controlled by authoritarian regimes. A privately issued currency responds to market incentives and is less likely to be co-opted to violate financial privacy and enact financial repression.

The most notable flatcoin in development is Nuon, currently still on Testnet (being experimented on), and unavailable to users. Nuon is overcollateralized with crypto assets and uses inflation data to maintain a peg at the price of a basket of goods. As stated in the Nuon whitepaper:

Just as decentralized protocols are the answer to risks posed by centralized currencies, and overcollateralization is the answer to maintaining value in the face of a market crash, inflation-proof flatcoins are the solution to preserving value over time.

Nuon’s flatcoin reflects an ambitious undertaking. Although developers appear to have learned their lesson from algorithmic stablecoin failures by overcollateralizing the asset, flatcoins face the same risks as other DeFi projects. For example, if the oracle their protocol relies on for inflation data is hacked or fails, chaos would ensue, similar to a compromise of Bloomberg or ICE data in traditional finance.

Bloomberg Galaxy Crypto Index vs. US CPI yoy (5 Years)

As entrepreneurs build the future of money, it makes sense to fully decouple from national currencies managed by central bankers. The brilliance of money not only as a medium of exchange, but as a good that evolves within a competitive marketplace, is clearly demonstrated here: inflation hitting 40-year highs has engendered an entrepreneurial response. If successfully developed, flatcoins will join the ranks of other digital assets like Bitcoin, providing individuals and institutions with monetary solutions outside fiat currencies. And if successful, this stage of innovation will add the preservation of purchasing power to the range of capabilities already available within the crypto space.

Related Posts

Operation Chokepoint 2.0: The Crypto Crackdown Explained (Video)

In this episode of Liberty Curious, Kate Wand discusses the Obama-era Operation Chokepoint, and today’s “Operation Chokepoint 2.0” with AIER Senior Research Faculty Thomas Hogan. Tom explains how government regulators […]

Earth Day, Waste and Productive Complements

It has been just over half a century since the first Earth Day in 1970. Over that time, April 22 has turned into a day with lots of waste cleanup […]

Focusing Exclusively on “Creating Jobs” Can Do More Harm Than Good

We are constantly bombarded by politicians declaring the importance of “creating jobs” in the economy. We regularly see government initiatives like public works projects, “stimulus” programs, and government subsidies enacted […]