Will the economy grow or shrink in 2023? That is the trillion-dollar question. Some say shrink, some say grow, but maybe the smartest of all say “I dunno.”

Soon after the Global Financial Crisis of 2008-9, then Wall Street Journal reporter Simon Constable and I teamed up to write a book for investors about the 50 most important economic indicators. Some readers complained that 50 indicators were too many to track, but others responded to our view that any modern economy, especially that of the United States, is too complex to understand by looking at just a few indicators, especially when major structural shifts are underway.

Our notion was that investors can “beat the market” by not getting beat by it. In other words, above-average risk-adjusted returns can be yours if you simply ride the high tide with everyone else, but jump ship into safer asset classes when you see the tide turning before others do. That means, though, that investors have to pay close attention to all of the sundry warning signals that an economy in trouble cannot help but emit, though it does not always do so clearly or unequivocally.

Fast or mechanical rules may deceive, because every variable must be understood in context. For a long time, for example, burlap orders were key because furniture manufacturers shipped their wares, which as consumer durables were highly correlated to the business cycle, covered in burlap. As burlap lost favor with shippers, though, the economic predictive power of burlap orders waned. More recently, corrugated cardboard orders serve a similar role, but you would have missed the recession of 2020 if you thought the economy was booming because Amazon et al ordered a bunch of cardboard shipping boxes as lockdowns spread across the country and globe.

AIER’s Pete Earle recently gave us an excellent example of the importance of understanding the numbers behind the numbers. Although real GDP rose 2.9 percent in the fourth quarter of 2022, beating consensus expectations of 2.6-2.7 percent, most of the gain came from reduced imports, not higher exports, and increased inventories, which could just as easily indicate unsold goods piling up as it could mean businesses stocking up in anticipation of banner sales in 2023.

Various organizations, including AIER, try to simplify economic forecasting by publishing or selling their own indices. The Conference Board, for example, revised its Leading Economic Index (LEI) on 1 February. A composite of 10 leading indicators, the LEI is down 3.8 percent since June 2022 and over 6 percent over the last year, clearly flashing “recession.” If you dig deeper into the numbers, though, as Earle did with GDP, perhaps the LEI should be giving even stronger indications of recession.

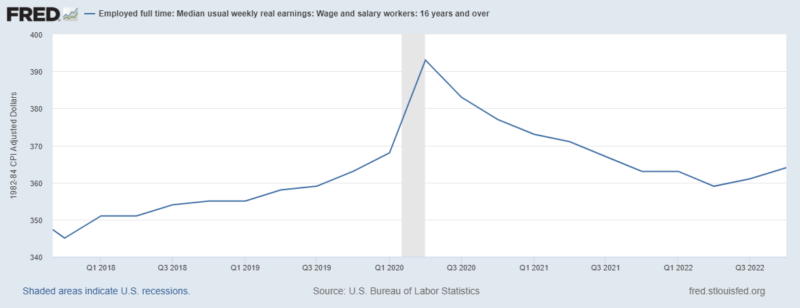

Consider, for example, average weekly initial claims for unemployment insurance, which is down slightly (and hence signaling a positive for the economy). The issue here is that the labor market has been behaving in an unusual fashion since the start of the pandemic: quiet quitting/resenteeism, record numbers of unfilled jobs, quiet hiring, a labor force participation rate that is improving but still below its pre-pandemic level, disability up at about 33 million, and so forth. The most palpable aspect of the current labor force situation, though, is that wages have not kept up with inflation, which is to say, in the parlance of economists, that real wages are down quite a bit:

Only a few people are losing their jobs, hence the unfilled jobs stats, but many workers are merely “filling positions” instead of “creating value” and, on average, they are taking home less purchasing power. Which is worse for the economy: joblessness, or workers pretending to work for pretend pay?

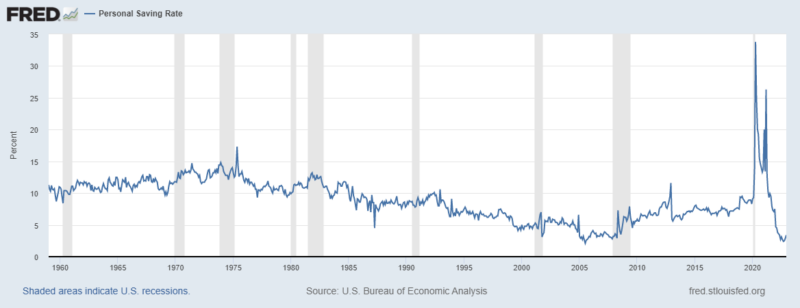

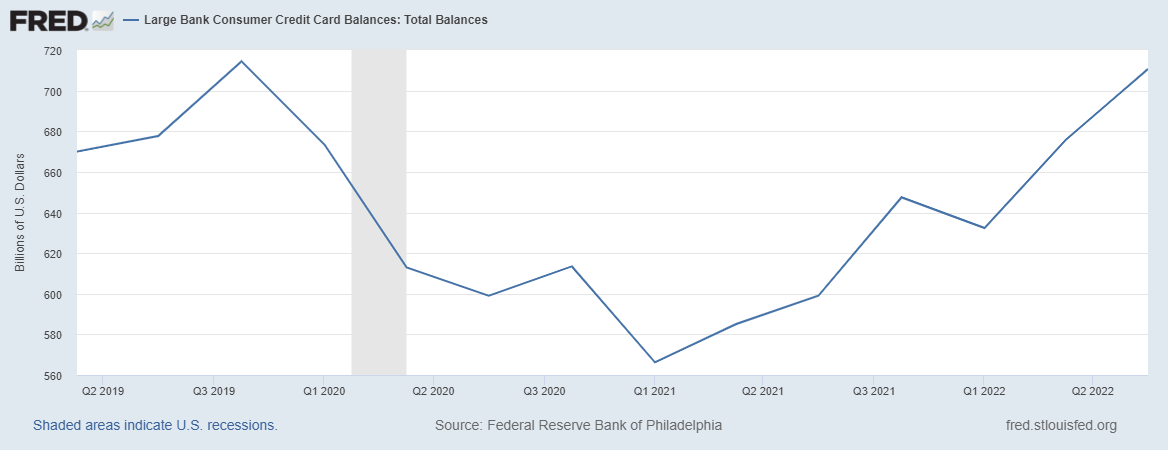

I don’t know, but I do know that the personal savings rate is at a 60-year low and credit card debt is through the roof.

Apparently, I am not the only one who burned through his liquid savings, stopped paying into his 401K, and ran up card balances in 2022.

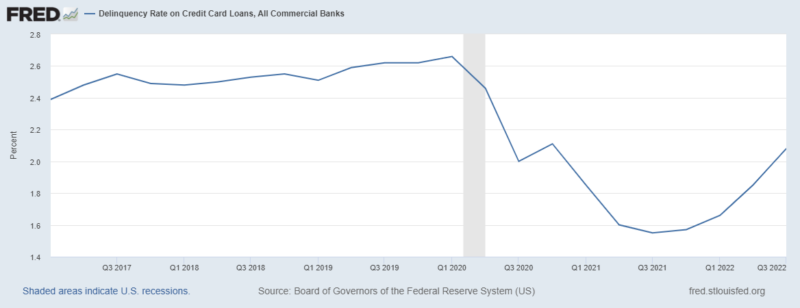

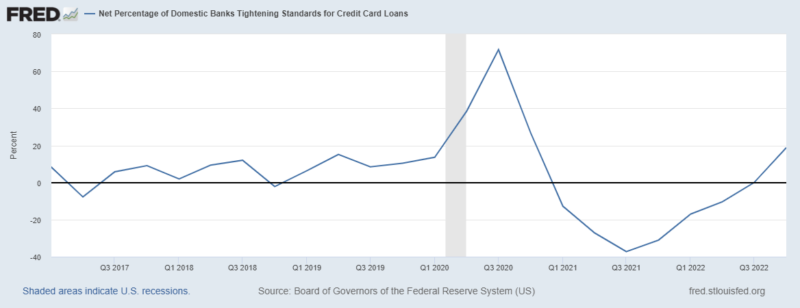

Credit card default rates are below their pre-pandemic level, but trending strongly upward.

Card issuers are already tightening standards.

Automobile loan defaults are up too, especially among the youngest borrowers.

This all suggests that although consumers expect much worse business conditions in the near future, as the LEI shows, they still might be too optimistic. Surveys are notoriously bad because respondents have no skin in the game and hence may answer based on what they think the pollster wants to hear. Although this is a long-standing issue, it may have gotten worse over the last few years as partisanship has gripped the nation’s political discourse and people rightfully fear social or economic retribution for sharing disfavored views. Even if they respond truthfully, people’s views might be skewed more than in the past due to the rampant dissemination of economic disinformation on traditional and social media. (See the debate over the definition of recession in the summer of 2022 for some insights into the extent of this emerging problem.)

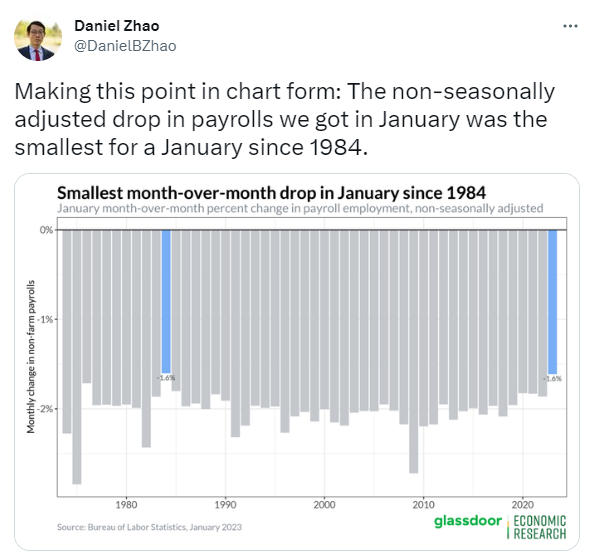

Case in point: Many Americans may actually believe that the US economy added jobs in January 2023 because of the Department of Labor posting dismisinfoganda like this on its website:

In fact, the reported numbers are seasonally adjusted. What actually happened is that the economy shed fewer jobs than in a typical January.

Journalists and social media bulls (or dollar bears) who want the Fed to stop increasing interest rates don’t add that crucial context, though, inducing people to think everything is just dandy.

The S&P Index is another component of the LEI. The stock market is a great leading indicator, as stock prices are theoretically just the discounted present value of expected future earnings. It is up ever so slightly but in real terms it, like wages, is actually down considerably since its December 2021 high.

Moreover, the S&P trends upwards over long periods, which is why investment advisors suggest buying stocks, especially when investors are young. But part of the reason that it trends upward is because most Americans have few other choices when it comes to their retirement savings. Sure, there are bonds and REITS and such but every week, week after week, the bulk goes into the same 500 “stonks.” In short, the stock market doesn’t just reflect expected future earnings, it also reflects expectations about future stock prices going up, simply because there aren’t many viable alternatives.

The expectation of future stock prices independent of earnings increased recently with the passage of Secure 2.0 as part of the 2022 Omnibus monstrosity. That part of the bill mandates that employers automatically enroll workers in 401Ks starting in 2025. Moreover, contributions must increase one percent annually until they reach at least 10 percent. Workers can opt out, so this is, for now, a nudge policy rather than forced savings, but it’s well understood that most workers will not, in fact, bother to unenroll, at least at first.

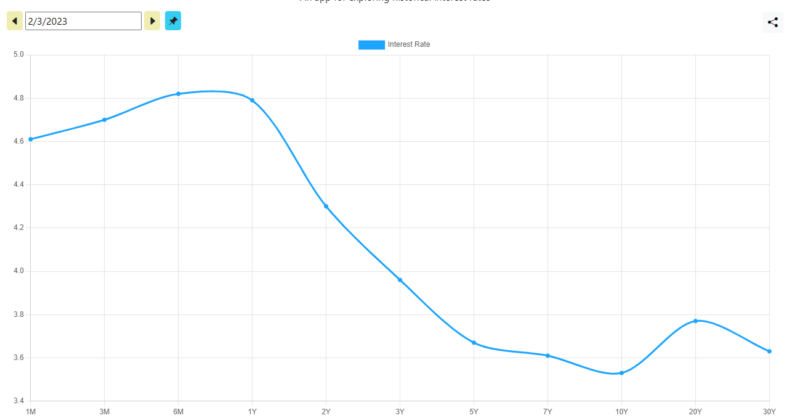

The LEI contains two other financial indicators, something called the Leading Credit Index, and a rough measure of the yield curve (10-year Treasury yields minus the federal funds rate). Inversion of the yield curve (short term yields > long term yields on bonds of comparable default and liquidity risk) has long been a tried and true recession indicator. The Treasury yield curve has been inverted for some time but in a unusually kinked fashion that the LEI’s simple measure does not capture:

The shape of the curve would traditionally have been taken to mean that bond-buyers think the economy is going to be flat in 2023 before heading downward in 2024. Maybe, though, the government is manipulating the curve (deliberately or not), or maybe bond buyers are also having a difficult time figuring out the US economy’s future direction. It is almost as if they are waiting to see if some big event, perhaps a war or AI boom, will occur.

Composed of six indicators, including some interest rate spreads and some surveys of bank loan officers and investors, the Leading Credit Index is slightly negative. The tricky thing is weighting the six indicators properly, given rapidly changing structural conditions like the increased use of AI in lending and investment decisions. AI, or ChatGPT anyway, is of no use divining what the right weights should be. When I queried what America’s real GDP growth rate would be this year, it responded:

Private Housing Building Permits, another component of the LEI, are also down. Perhaps it is also a bit too optimistic when viewed in context. New housing starts were down even more than permits in 2022, suggesting that the permit drop lag rate (permits pulled but unused for longer than usual) has increased, likely due to recession fears and higher interest rates.

The remaining four components of the LEI – the ISM New Order Index, average weekly hours of manufacturing workers, non-defense, non-aircraft capital goods orders, and consumer goods orders – all relate to the manufacturing sector. They are all down or flat, indicating that the next quarter cannot be good. New orders can turn quickly, but why should they, given that the US economy remains trapped between the Scylla of higher interest rates and the Charbydis of higher inflation?

In short, I would keep my eye on the LEI (and AIER’s equivalent) but pay special attention (overweight) to the manufacturing variables. Outside of the LEI, I would also carefully watch real wage trends and its downstream knockoffs (credit card and other debt and defaults, and the personal savings rate). Uncommon times call for uncommon measures.

Related Posts

Operation Chokepoint 2.0: The Crypto Crackdown Explained (Video)

In this episode of Liberty Curious, Kate Wand discusses the Obama-era Operation Chokepoint, and today’s “Operation Chokepoint 2.0” with AIER Senior Research Faculty Thomas Hogan. Tom explains how government regulators […]

Earth Day, Waste and Productive Complements

It has been just over half a century since the first Earth Day in 1970. Over that time, April 22 has turned into a day with lots of waste cleanup […]

Focusing Exclusively on “Creating Jobs” Can Do More Harm Than Good

We are constantly bombarded by politicians declaring the importance of “creating jobs” in the economy. We regularly see government initiatives like public works projects, “stimulus” programs, and government subsidies enacted […]